India’s steel industry is approaching a strategic crossroads. For decades, the country’s industrial rise has been built on blast furnaces fed by imported coking coal. But a new economic reality is emerging: the future cost of producing steel may increasingly depend not on coal imports, but on access to cheap solar power, green hydrogen and carbon-conscious export markets.

A recent analysis by researchers at the India Energy and Climate Center at the University of California, Berkeley argues that India could become one of the world’s cheapest producers of green steel within this decade.

The implications extend far beyond climate policy. At stake are India’s trade competitiveness, industrial energy security, export earnings and exposure to future carbon taxes.

India is already the world’s second-largest steel producer, manufacturing nearly 149 million tonnes of crude steel annually. The country plans to expand installed steelmaking capacity to 300 million tonnes by 2030-31.

Much of that expansion is still expected to rely on the conventional blast furnace-basic oxygen furnace route, which depends heavily on imported coking coal. The expansion strategy aligns with India’s long-term infrastructure ambitions, including highways, railways, urbanisation and manufacturing-led economic growth.

According to the World Steel Association, India has been among the fastest-growing steel markets globally over the past decade.

That model increasingly looks risky.

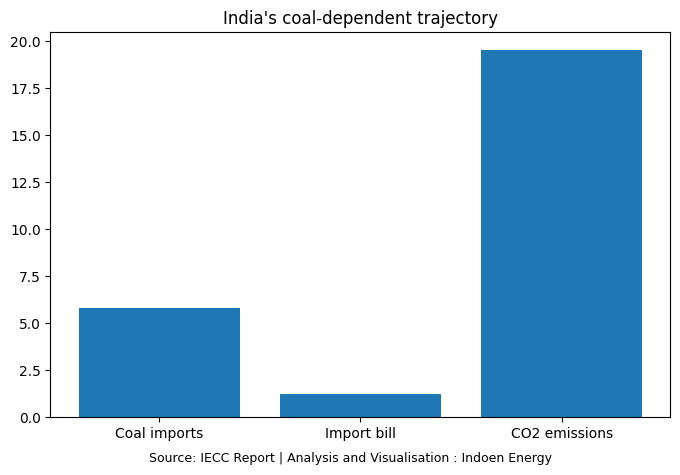

The Berkeley-backed assessment estimates that continuing with the existing trajectory could lock India into nearly 5.8 billion tonnes of cumulative coking coal imports over four decades, involving an import bill of roughly US$1.2 trillion and nearly 19.5 gigatonnes of committed carbon emissions.

The timing is crucial because the European Union’s Carbon Border Adjustment Mechanism (CBAM) formally entered its compliance phase in January 2026. Europe currently accounts for a significant share of India’s steel exports, and the new carbon pricing regime threatens to reshape global trade flows.

The mechanism is designed to impose carbon-linked costs on imported products with high embedded emissions. According to the European Commission’s CBAM framework, sectors including steel, aluminium and cement will face progressively stricter carbon accounting obligations during the transition phase.

Coal dependence becomes a strategic liability

India imports more than 90% of its coking coal requirements. This dependence has become increasingly expensive in recent years as global commodity markets turned volatile following the pandemic, the Russia-Ukraine conflict and disruptions in global shipping routes.

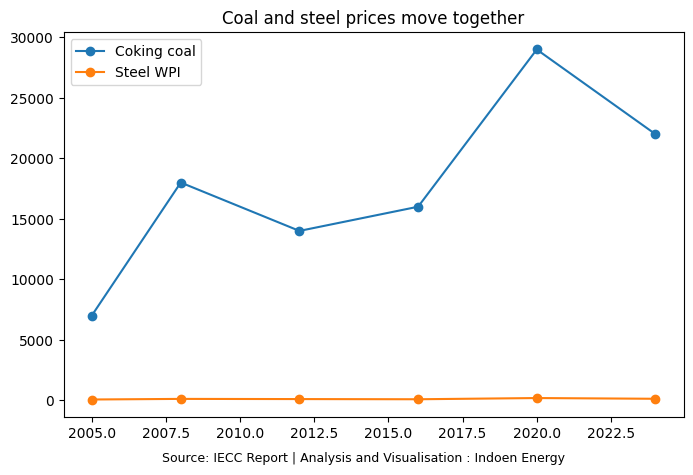

The report notes that imported coking coal prices and Indian steel prices have historically moved in close alignment, showing how international energy shocks quickly translate into higher domestic steelmaking costs.

Similar volatility has affected steelmakers globally since 2021, with coal and energy prices repeatedly disrupting industrial margins across Asia and Europe.

The deeper concern lies in currency exposure.

Since coal is purchased largely in US dollars, every depreciation of the rupee inflates conventional steel production costs.

The study estimates that the rupee has weakened against the dollar by an average of 3.2% annually over the past two decades, while seaborne coking coal prices rose around 4.2% annually in nominal dollar terms during the same period. Combined, this produced a 7.4% yearly escalation in rupee-denominated coal costs for blast furnace-based steelmaking.

Green steel follows a different cost structure. In hydrogen-based steel production, green hydrogen replaces coking coal as the primary reducing agent.

Since that hydrogen is produced using renewable electricity sourced domestically through long-term power purchase agreements, much of the energy cost can remain locked in rupee terms for decades. This potentially shields green steel producers from the imported fuel volatility that affects coal-dependent steel plants.

That distinction may fundamentally alter steel economics over the coming decades.

Green hydrogen begins to look commercially viable

The conventional criticism of green steel has always centred on cost. Hydrogen-based steelmaking was considered technologically promising but commercially unrealistic.

That equation may now be changing rapidly.

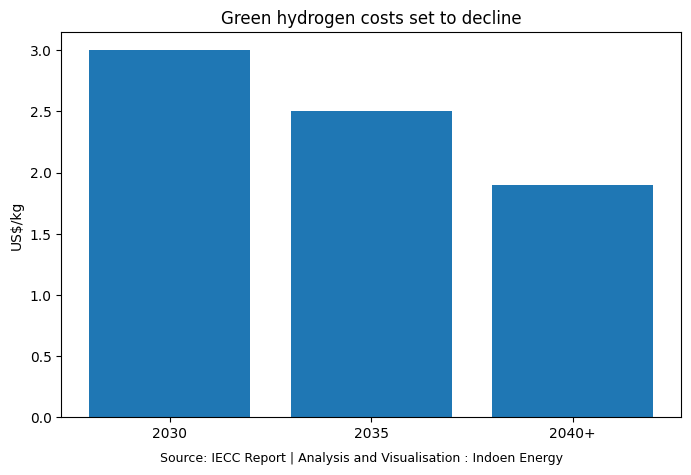

The study estimates that green hydrogen production costs in India could fall to around US$3 per kilogram by 2030, driven largely by low-cost solar electricity and falling electrolyser costs. India’s policy ecosystem is also evolving rapidly around hydrogen deployment. The National Green Hydrogen Mission aims to position India as a global production hub through subsidies, electrolyser manufacturing incentives and export-oriented industrial policies.

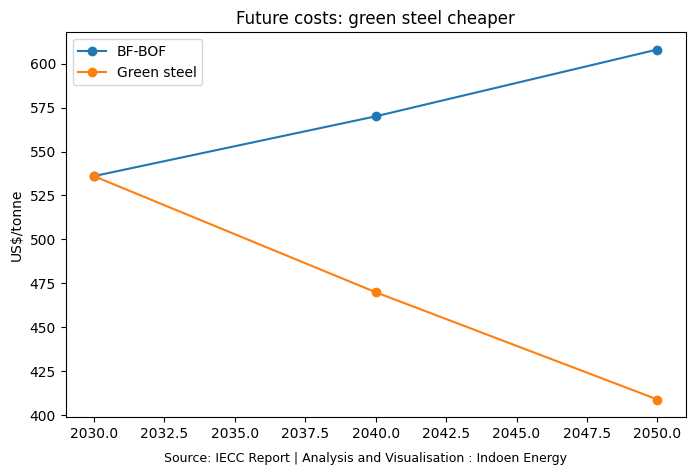

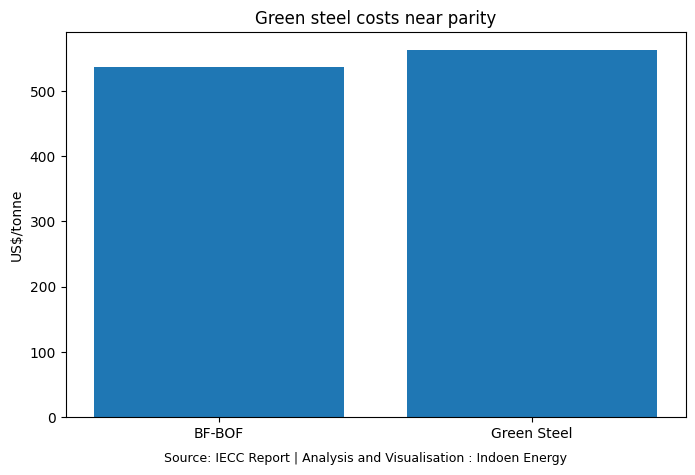

At that hydrogen price, green steel produced through hydrogen-based direct reduced iron and electric arc furnaces could cost roughly US$562 per tonne — only around 5% higher than conventional new blast furnace-based steel production.

More importantly, researchers argue that once future coal inflation, currency depreciation and carbon border taxes are considered, green steel could actually become cheaper than new coal-based steel plants by the early 2030s.

Several global consulting firms and energy analysts are reaching similar conclusions.

Firms such as RMI, EY-Parthenon and CEEW have all projected a rapid narrowing of the green steel cost premium during the 2030s. Recent analysis from Rocky Mountain Institute similarly argues that falling renewable energy and electrolyser costs could fundamentally reshape industrial competitiveness in steel manufacturing.

The dramatic fall in renewable energy prices has accelerated this shift. India already hosts some of the world’s cheapest solar tariffs, aided by strong irradiation levels across Rajasthan, Gujarat and western India. The report argues that India’s geographical advantage near the equator allows relatively stable solar output throughout the year, reducing the storage requirements needed for round-the-clock hydrogen production.

Recent hydrogen and ammonia auctions have reinforced optimism. Some Indian auction-discovered hydrogen prices are already approaching the US$3.5 per kilogram range after accounting for incentives and transmission benefits.

Meanwhile, the International Energy Agency’s hydrogen market review notes that Asia is likely to become one of the largest future hydrogen demand centres due to industrial decarbonisation pressures.

Europe’s carbon tariffs could reshape steel trade

The EU’s CBAM may ultimately become the strongest commercial driver for India’s green steel transition.

Europe imports billions of dollars worth of Indian iron and steel annually. However, CBAM will progressively impose carbon-linked costs on imported steel products that do not meet Europe’s decarbonisation standards.

The Berkeley analysis estimates that under a carbon price of around US$85 per tonne of CO₂, conventional blast furnace steel from India and China could become significantly more expensive in European markets than green steel produced through hydrogen-based routes.

One estimate cited in the report suggests Indian steel exporters could face additional CBAM-linked costs of around US$237 per tonne by 2030 and as much as US$638 per tonne by 2040 if production remains carbon-intensive.

That could dramatically alter investment decisions inside India’s steel sector.

“Companies building conventional blast furnaces today may discover that these assets become economically stressed much earlier than expected,” said an executive at a Mumbai-based clean energy consultancy working with industrial decarbonisation projects.

Meanwhile, Indian companies are already exploring low-carbon pathways. Firms including Tata Steel, JSW Steel and ArcelorMittal Nippon Steel India have announced pilot initiatives involving hydrogen, renewable integration and carbon reduction technologies. India’s Ministry of Steel has also been discussing green steel taxonomy frameworks and procurement incentives aimed at accelerating adoption.

Globally, the race is intensifying. Sweden’s HYBRIT project, Germany’s industrial hydrogen push and large-scale investments across Spain and the Middle East are positioning green steel as the next major industrial battleground.

India’s solar advantage could become an industrial advantage

Unlike Europe or Japan, India combines three major advantages rarely available together: abundant solar potential, relatively low labour costs and access to substantial iron ore reserves.

The report argues that Indian iron ore costs remain competitive internationally because of relatively high-grade domestic reserves.

That combination could allow India not merely to decarbonise its steel sector, but potentially emerge as a leading exporter of low-carbon steel and green iron products.

There is also a geopolitical dimension.

Reducing coking coal imports would help India lower vulnerability to global commodity shocks and reduce pressure on foreign exchange reserves. India’s annual coking coal import bill could eventually approach US$30 billion annually under the current expansion pathway.

At a time when countries are increasingly viewing industrial supply chains through the lens of strategic autonomy, green steel may become as much a security issue as an environmental one.

The broader decarbonisation push is also reshaping industrial policy worldwide. The International Energy Agency’s steel technology roadmap argues that low-emission steel production will become central to future manufacturing competitiveness, particularly as advanced economies tighten climate-linked trade regulations.

The transition still faces major obstacles

The transition still faces major obstacles

Yet the green steel transition remains far from guaranteed.

Hydrogen infrastructure is still limited. Electrolysers remain expensive. Financing first-generation projects continues to be difficult. Large-scale renewable integration into industrial clusters poses major grid challenges.

Critics also argue that green hydrogen economics remain heavily dependent on policy support and falling technology costs that may not materialise as quickly as projected.

Others point out that carbon capture technologies for conventional steel plants could remain cheaper in certain contexts.

The Berkeley study itself acknowledges that large-scale deployment will require government support mechanisms including procurement mandates, long-term offtake agreements, risk-sharing frameworks and clear green steel certification systems.

Still, momentum appears to be building globally.

As investors, export markets and regulators increasingly price carbon into industrial supply chains, the economics of steel production may no longer be determined solely by cheap coal.

India’s steel industry now faces a historic question: whether to continue building around imported fossil fuel dependence, or pivot towards a new industrial model powered by domestic renewable energy.

The answer could shape not only India’s climate trajectory, but also its position in the future global manufacturing order.