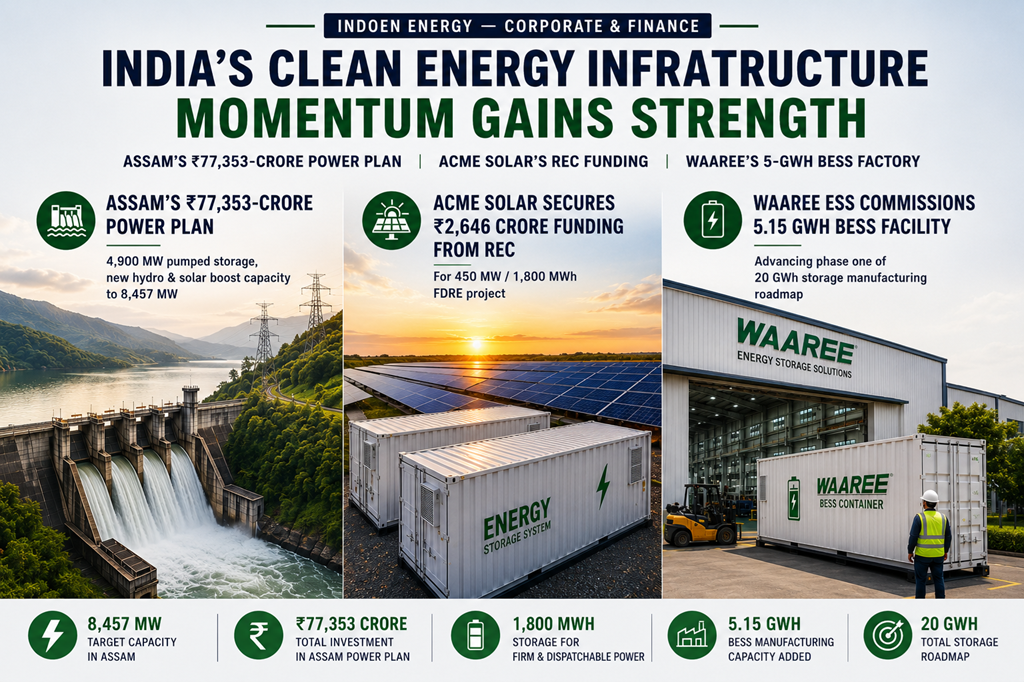

India’s renewable energy transition is entering a new phase — one where electricity storage, rather than generation capacity alone, may determine the pace and stability of the country’s clean energy ambitions.

A series of recent developments across India’s battery energy storage system (BESS) sector suggests that storage is rapidly evolving from a niche balancing technology into a strategic layer of national energy infrastructure.

From Rajasthan’s push for decentralised battery deployment and Gujarat’s expanding storage network to new manufacturing investments and emerging battery recycling partnerships, the contours of a much larger industrial shift are beginning to emerge.

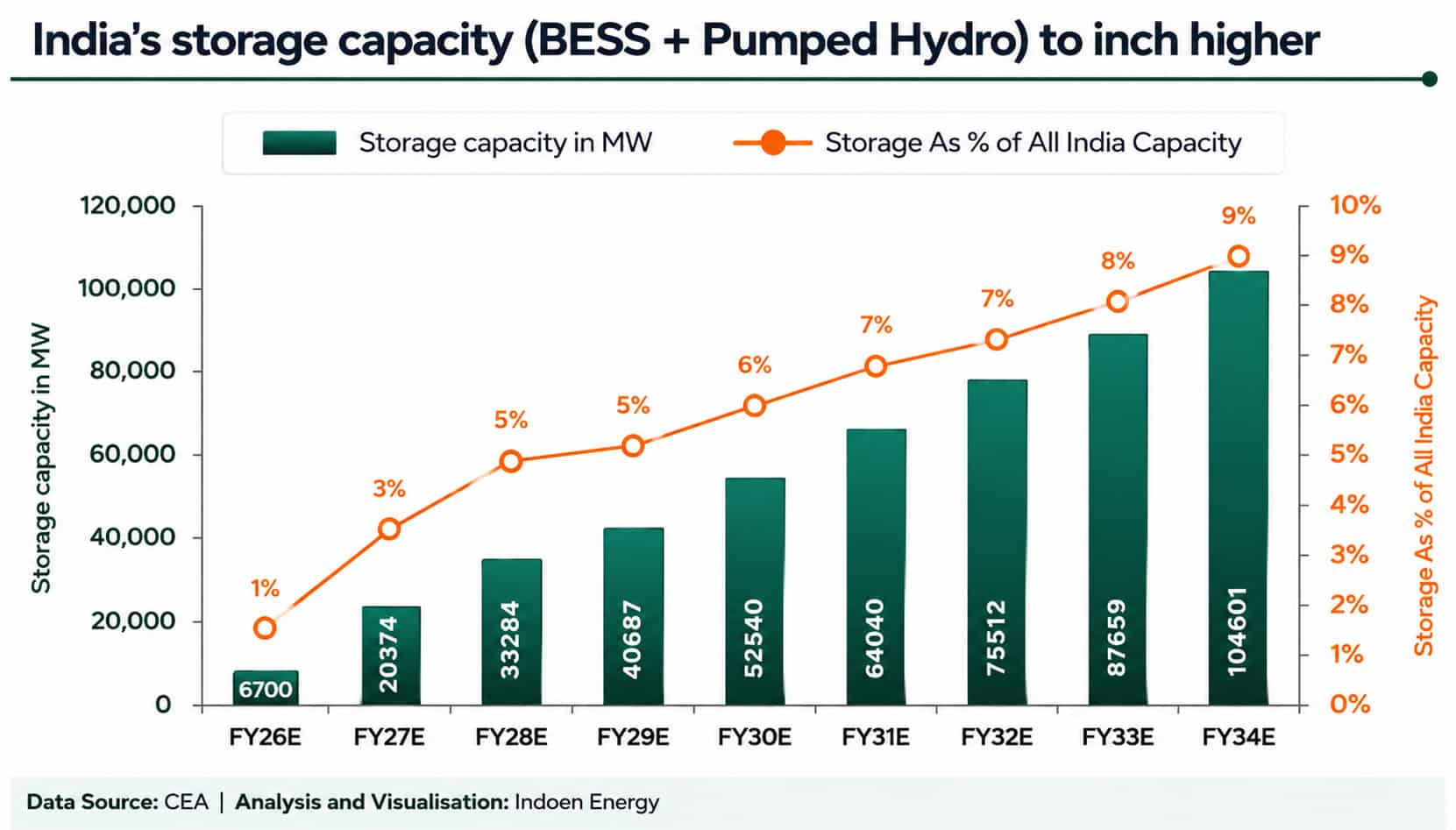

The transition is unfolding at a time when India’s renewable energy capacity is growing faster than the grid’s ability to absorb and distribute intermittent power reliably.

Solar and wind installations continue to surge, but the challenge of managing evening demand peaks, transmission bottlenecks and fluctuating generation is becoming increasingly visible across several states.

That is turning storage from a future technology into an immediate operational necessity.

Rajasthan, one of India’s largest solar-producing states, recently announced plans for decentralised battery storage deployment aimed at improving grid stability and enhancing renewable energy utilisation.

The move reflects a broader concern among state utilities and grid operators that large-scale renewable expansion without flexibility infrastructure could eventually create reliability risks rather than energy security gains.

The state’s guidelines for integrating battery storage with renewable energy systems indicate how policymakers are beginning to view storage not merely as backup power but as a core component of future grid architecture.

Hybrid renewable-plus-storage systems are increasingly being seen as essential for reducing curtailment and smoothing power supply variability.

The shift is not limited to Rajasthan. Gujarat has also accelerated battery deployment, including plans linked to an 870 MW storage network intended to stabilise the state’s power system amid rising renewable penetration.

These developments reveal an important underlying trend: India’s energy transition is gradually shifting from a generation story to a flexibility story.

For years, policy discussions focused heavily on adding renewable capacity. However, as solar and wind power occupy a larger share of the electricity mix, the system’s ability to store, dispatch and balance electricity is emerging as the next major challenge.

Industry executives increasingly argue that India’s ‘second-generation’ energy transition will revolve around storage, transmission modernisation and grid intelligence rather than renewable installation alone.

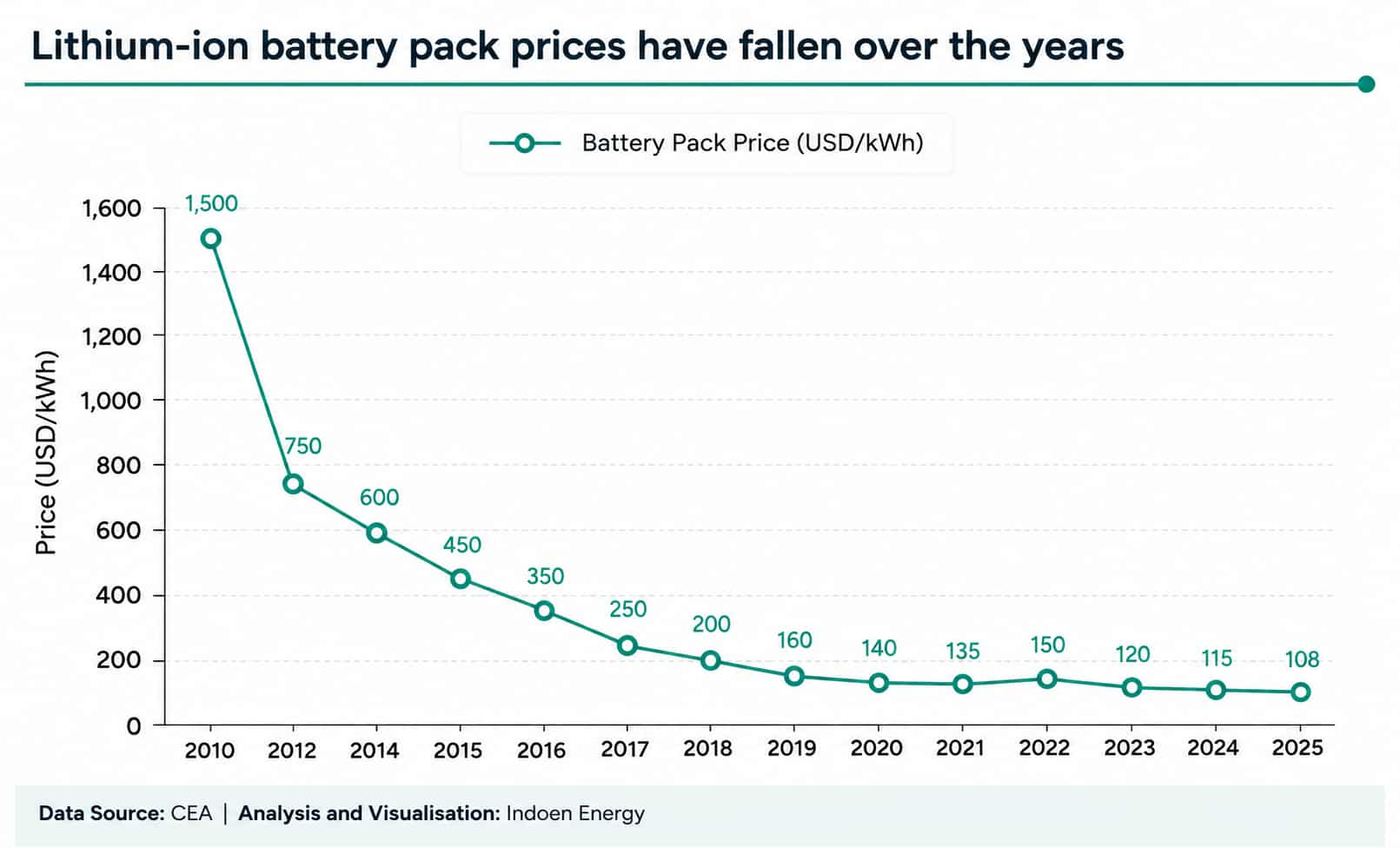

Falling battery prices alter the economics

The economics are also changing rapidly.

Global lithium-ion battery prices have fallen sharply over the past decade, driven largely by China’s manufacturing scale-up and the growth of the electric vehicle market. According to BloombergNEF, battery pack prices reached record lows in recent years, making large-scale storage increasingly commercially viable for utilities and industrial consumers alike.

This has opened the door for a wider transformation of India’s power ecosystem.

One of the most significant signals comes from the manufacturing side.

Indian solar manufacturer Solex Energy recently announced plans to establish a 10 GW battery storage manufacturing facility alongside a 5 GW solar cell plant in Gujarat.

The announcement highlights how Indian firms are beginning to see storage manufacturing as a long-term industrial opportunity rather than a peripheral clean-energy business.

That could have major economic implications.

For much of the past decade, India’s renewable expansion depended heavily on imported solar modules and battery components, particularly from China. Policymakers now appear increasingly determined to avoid repeating the same dependence pattern in storage technologies.

The geopolitical battle behind batteries

This is where the story becomes geopolitical.

The global battery supply chain is currently dominated by China across refining, processing and cell manufacturing. Beijing controls significant portions of the lithium, cobalt and graphite processing ecosystem that powers the modern battery economy.

As countries compete to secure energy transition supply chains, batteries are becoming strategically comparable to oil infrastructure in earlier decades.

India’s efforts to build domestic manufacturing capacity therefore reflect not only climate ambitions but also concerns around industrial competitiveness, supply security and technological sovereignty.

Yet building a domestic battery ecosystem will not be easy.

India still faces substantial gaps in upstream mineral access, advanced cell chemistry expertise and large-scale processing capabilities. Financing remains another major challenge. Utility-scale battery projects require high upfront investments, while revenue models for storage services are still evolving.

Some sector analysts also caution that India’s regulatory framework for storage deployment remains fragmented across states. Questions around tariff structures, ancillary service markets and long-duration storage incentives are still being debated.

Nevertheless, the direction of travel appears increasingly clear.

EV charging and storage begin to merge

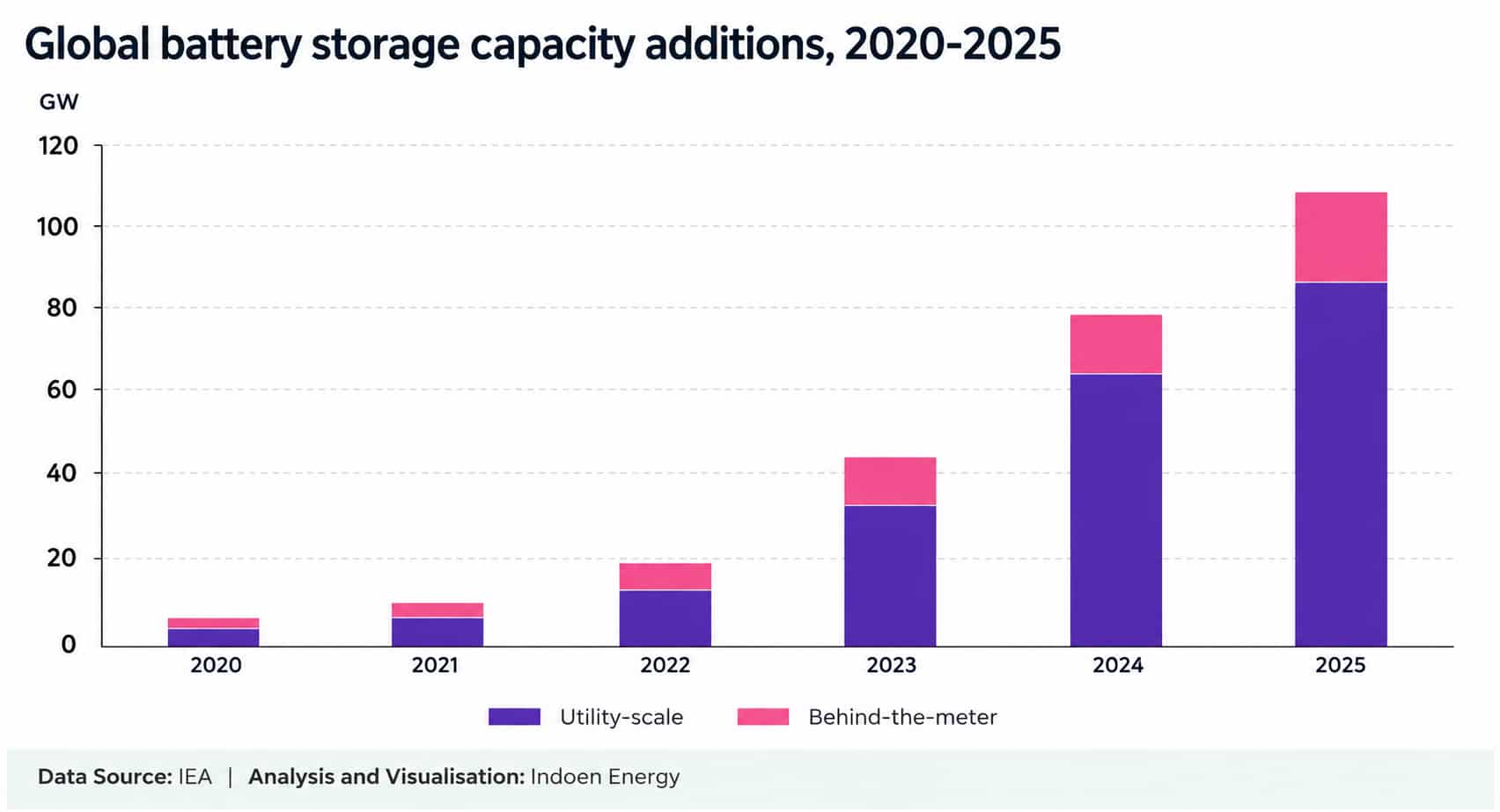

Another emerging trend is the convergence between battery storage and electric mobility infrastructure.

Globally, battery-integrated EV charging hubs are beginning to play a larger role in managing grid stress and reducing peak electricity costs. A recent industry assessment showed that BESS-linked EV charging projects have already crossed 1 GWh in several major markets, while China is reportedly planning deployments exceeding 10 GWh.

This convergence could eventually reshape India’s urban energy systems.

Battery-supported charging infrastructure may allow high-speed charging corridors, commercial fleet depots and urban charging hubs to operate without placing excessive pressure on local distribution networks. In cities already struggling with peak demand stress, storage-backed EV infrastructure could become increasingly important.

The implications stretch beyond power management.

Recycling may become the next strategic frontier

One of the lesser-discussed realities of the global battery boom is that it could create a new form of resource dependence. Countries moving away from fossil fuels may find themselves increasingly reliant on critical minerals such as lithium, nickel and cobalt.

That has pushed recycling into the centre of strategic policy discussions.

The European Union and India recently launched a joint initiative worth approximately €15.2 million focused on battery recycling and electric vehicle waste management.

The initiative reflects growing recognition that the future battery economy will not depend solely on manufacturing capacity but also on circular supply chains.

Industry experts increasingly describe used batteries as a form of ‘urban mine’ capable of recovering valuable minerals and reducing future import dependence.

This could become one of the most strategically important yet underdeveloped segments of India’s clean-energy economy.

The next phase of India’s energy transition

The next phase of India’s energy transition

The scale of future demand is substantial. India’s electricity consumption is projected to rise sharply over the coming decade, driven by industrialisation, urbanisation, air-conditioning demand and the expansion of digital infrastructure such as AI-linked data centres.

That creates a paradoxical challenge for the energy transition.

Renewable energy capacity may continue growing rapidly, but without parallel investments in storage and grid flexibility, system instability risks could also increase. Several countries, including parts of Europe and California in the United States, have already experienced the operational complexities of managing high renewable penetration without sufficient balancing infrastructure.

India may therefore be approaching a decisive turning point.

The first phase of the energy transition focused on building renewable generation capacity. The next phase may revolve around ensuring that clean electricity remains dispatchable, stable and economically usable at scale.

In that context, battery infrastructure is no longer merely supporting the transition. It is becoming central to how the transition itself functions.

And unlike the solar boom, where manufacturing leadership consolidated rapidly in a handful of countries, the global storage race remains more fluid. That gives India a narrow but significant window to build industrial capabilities before supply chains become permanently entrenched elsewhere.

Whether India can translate policy ambition into a globally competitive battery ecosystem will depend on financing reforms, mineral access strategies, domestic manufacturing depth and regulatory clarity.

But one thing is becoming increasingly difficult to ignore: the future battle over energy dominance may not be fought only through generation capacity, but through who controls flexibility, storage and the infrastructure that keeps renewable-heavy grids running reliably.