India’s electricity market is entering a phase few policymakers had fully anticipated. In different parts of the country, power prices are now crashing to near-zero levels during some hours of the day, only to spike sharply a few hours later despite record renewable energy additions and rising generation capacity.

The volatility marks a structural shift in how electricity is being produced, traded, transmitted, and consumed in the country. India’s power system, once dominated by predictable coal generation and relatively stable demand patterns, is increasingly behaving like a real-time balancing market shaped by weather conditions, transmission bottlenecks, renewable intermittency and changing consumption patterns.

The result is a paradoxical electricity economy where India can simultaneously experience renewable energy wastage, regional shortages, stressed distribution companies and rising consumer bills.

The shift could redefine how India thinks about energy security, grid infrastructure, storage investment and electricity market design over the next decade.

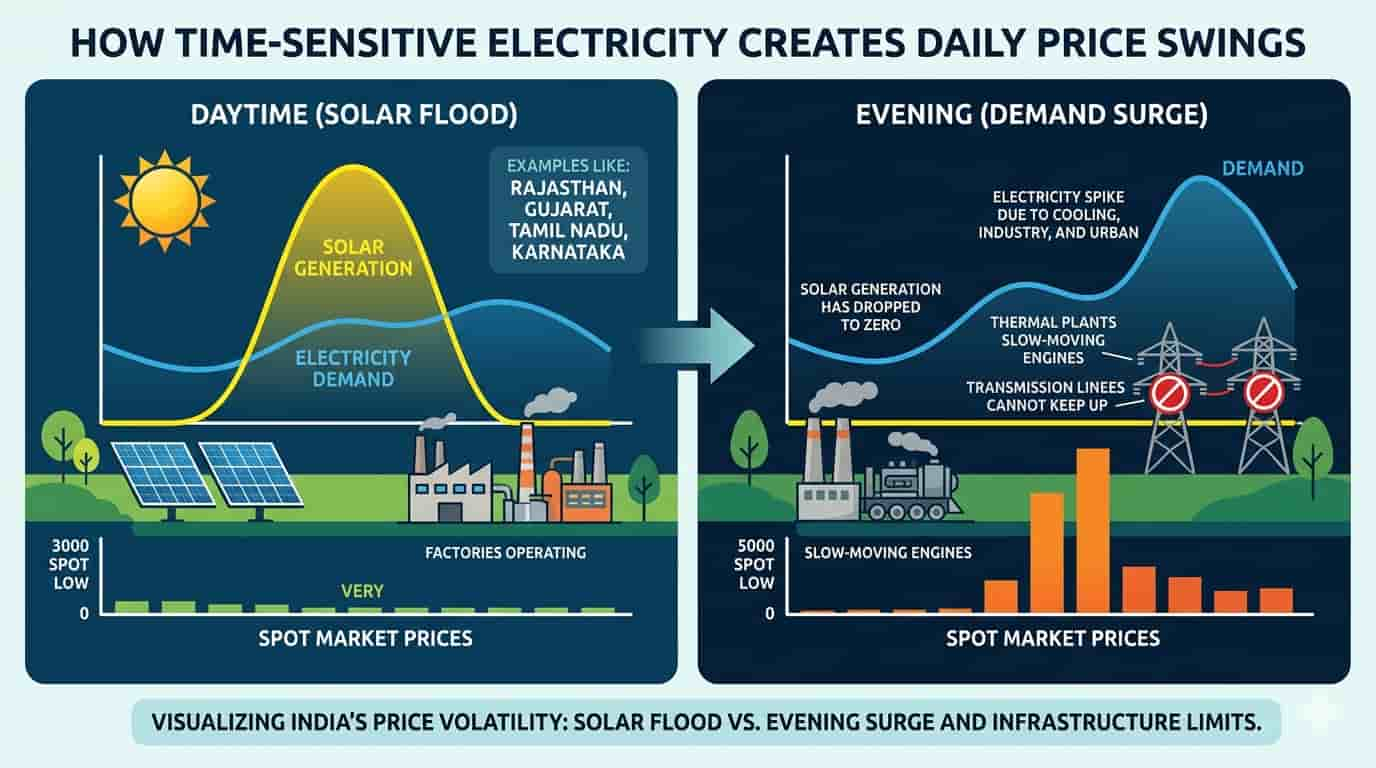

India’s power exchanges have already begun reflecting this new reality. Spot market prices on the Indian Energy Exchange (IEX) have periodically collapsed to near-zero levels during periods of high solar generation, even as peak evening prices continue to rise during periods of intense demand.

This emerging volatility is no longer a temporary market distortion. It increasingly reflects the changing physics and economics of India’s electricity system.

The paradox of surplus and shortage

For decades, India’s electricity sector was largely built around controllable thermal generation. Coal plants operated steadily, demand patterns remained relatively predictable and utilities managed supply centrally.

That framework is now under pressure.

Solar generation floods the grid during daylight hours, particularly in states with high renewable penetration such as Rajasthan, Gujarat, Tamil Nadu and Karnataka. During these periods, supply often exceeds immediate demand in regional markets, pushing spot prices sharply downward.

But after sunset, when solar generation rapidly falls, electricity demand frequently remains elevated due to cooling requirements, industrial activity, and urban consumption. Thermal plants are often unable to ramp up quickly enough, while transmission limitations prevent surplus electricity from moving efficiently across regions.

This creates sudden price spikes within the same day.

The phenomenon has become more pronounced amid rising summer temperatures and increasing air-conditioning penetration across India. Peak electricity demand crossed 270 GW recently, with officials expecting demand to continue climbing as urbanisation, electric mobility, data centres, and digital infrastructure expand.

Industry executives say India’s power market is gradually shifting from a generation-deficit system to a flexibility-deficit system.

That distinction matters.

The challenge is no longer simply producing electricity. It is increasingly about managing when power arrives, where it arrives, how fast it can move across the grid, and whether the system can absorb sudden fluctuations.

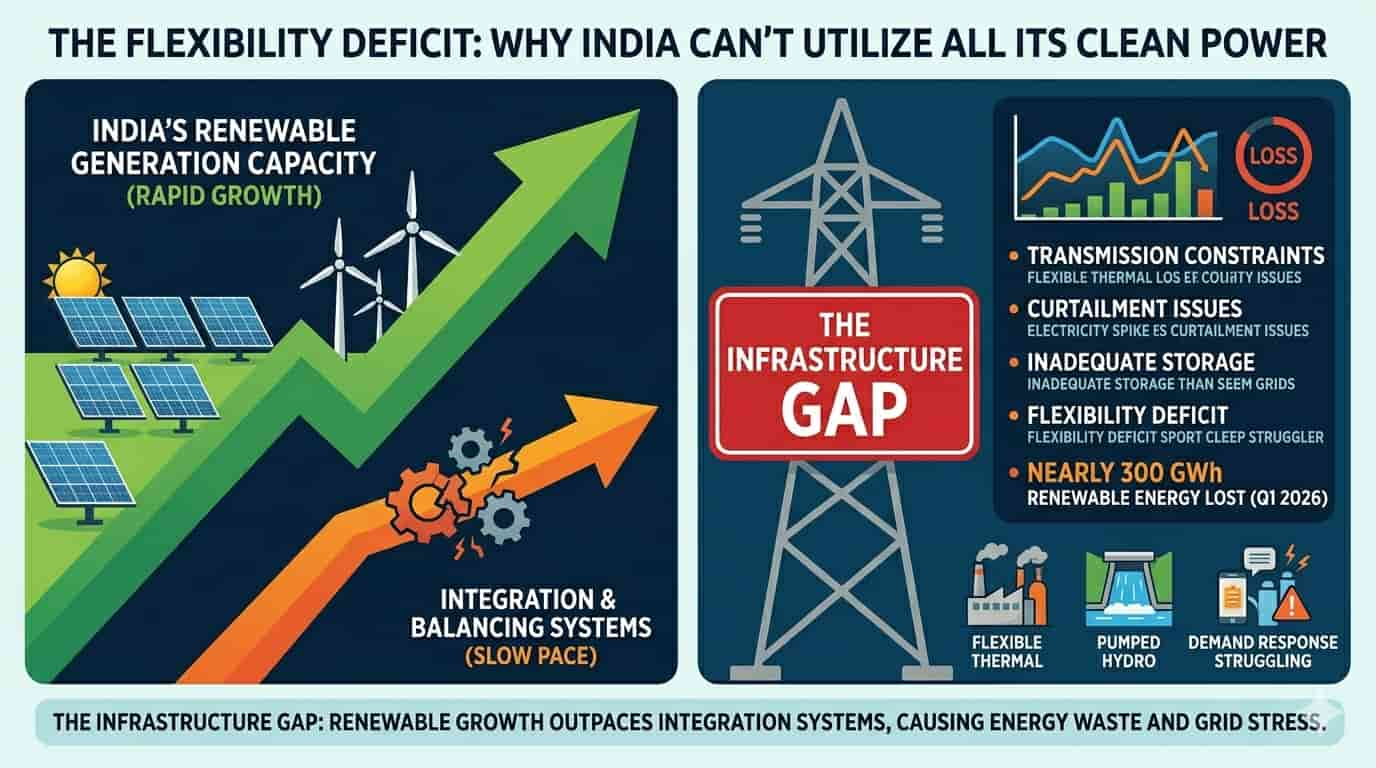

Renewable growth is exposing infrastructure gaps

India’s renewable energy expansion has been among the fastest in the world. The government continues to pursue ambitious clean-energy targets, including a broader vision of 1,500 GW of clean energy capacity highlighted recently by former NITI Aayog chief executive Amitabh Kant.

Yet the rapid pace of renewable deployment is increasingly exposing weaknesses elsewhere in the system.

India reportedly lost nearly 300 GWh of renewable energy in the first quarter of 2026 due to transmission constraints and curtailment issues.

This is becoming one of the most underappreciated features of India’s energy transition.

The country is adding renewable generation capacity faster than it is building the systems needed to integrate and balance that capacity efficiently.

Transmission networks, storage systems, flexible generation assets, ancillary services, forecasting systems and demand-response mechanisms are all struggling to keep pace.

In effect, India is entering an era where electricity prices are increasingly being shaped not only by fuel costs, but also by timing, geography, weather variability and infrastructure constraints.

This is beginning to resemble trends already visible in parts of Europe, California and Australia, where renewable-heavy electricity systems frequently witness negative prices during periods of excess generation and sharp evening spikes during periods of tight supply.

The rise of timing-sensitive electricity markets

One of the biggest changes underway is that electricity itself is becoming increasingly timing-sensitive.

A unit of electricity generated at noon during periods of high solar output may have far lower economic value than electricity available during evening peaks.

That is fundamentally changing investment calculations across the power sector.

Battery storage developers, pumped hydro operators, flexible gas generators and grid-balancing service providers are becoming increasingly important in electricity markets globally. India is beginning to move in the same direction.

Older Indoen Energy analyses have already explored how storage economics are reshaping energy markets and how India’s power system is gradually shifting towards flexibility-led infrastructure models.

But volatility in electricity prices suggests the transition may now be accelerating faster than anticipated.

Market analysts say price instability itself could become one of the biggest drivers of future battery storage investment in India. The more volatile electricity prices become, the greater the commercial value of storing cheap daytime electricity and discharging it during expensive evening peaks.

This dynamic is already transforming electricity markets internationally.

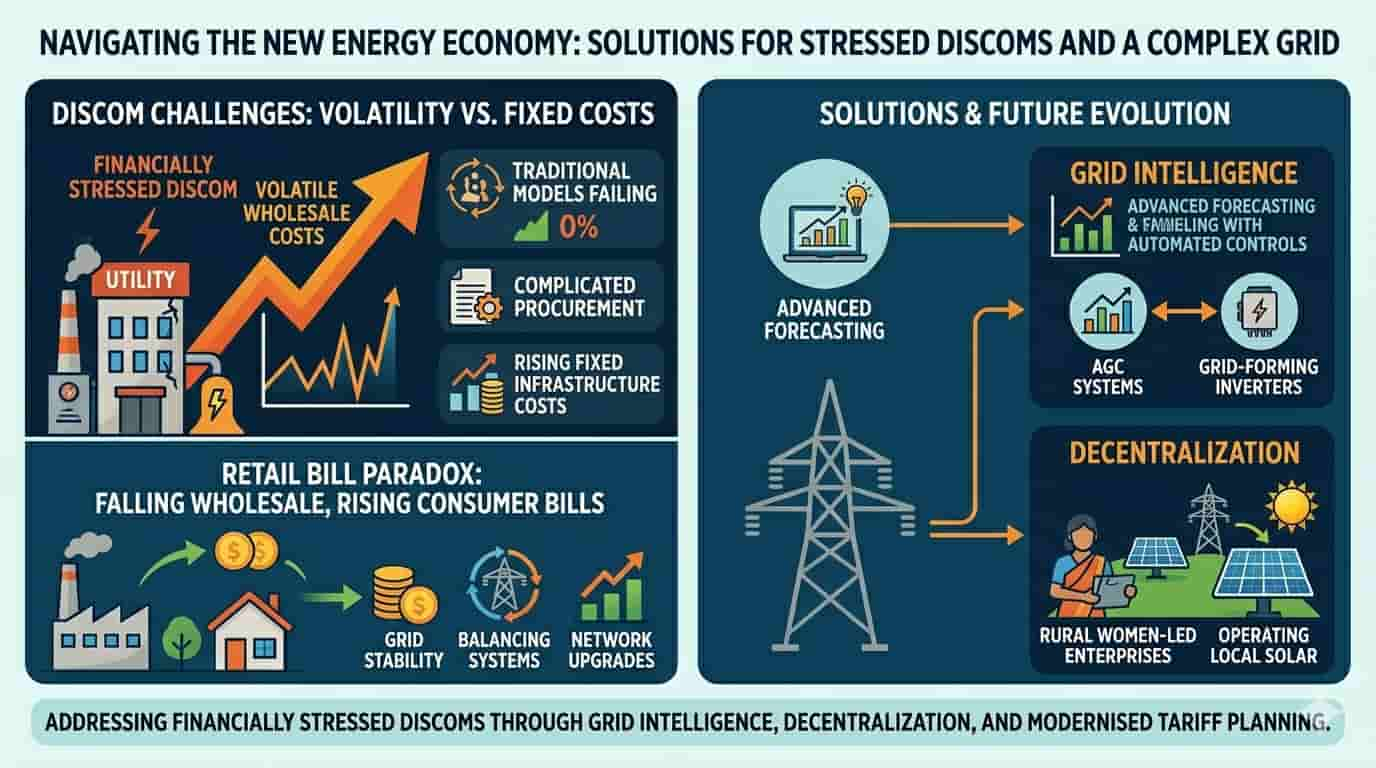

Discoms are entering a more difficult phase

The new volatility also creates deeper challenges for India’s financially stressed distribution companies.

Traditional discom business models were built around relatively predictable procurement costs and stable demand patterns. But increasingly volatile wholesale markets complicate purchasing strategies, tariff planning and system balancing.

At the same time, fixed infrastructure costs remain high even when renewable generation reduces energy procurement expenses. Several analysts argue that falling revenues, rising balancing costs, and cross-subsidy pressures are creating structural stress for discom finances.

This partly explains another paradox emerging in India’s electricity economy: wholesale prices may fall during some periods, yet retail electricity bills can still rise.

Consumers are paying not just for generation, but increasingly for grid stability, balancing systems, transmission infrastructure, reserve capacity and network upgrades.

The grid itself is becoming more complex

Managing large-scale intermittent generation requires a combination of faster balancing systems, advanced forecasting capabilities, automated grid controls, grid-forming inverters, real-time dispatch coordination and well-developed ancillary power markets to ensure grid stability, reliability and efficient integration of renewable energy sources.

The growing discussion around Automatic Generation Control (AGC) systems and grid-forming inverter technologies reflects how India’s energy transition is becoming as much a digital and systems-management challenge as an infrastructure challenge.

Grid resilience concerns are also becoming more prominent amid rising renewable penetration and increasingly extreme weather events.

In some ways, India’s electricity system is moving from an infrastructure problem to an intelligence problem.

The next phase of the transition may depend less on how many megawatts India builds and more on how intelligently the system coordinates supply, storage, transmission, and consumption in real time.

Decentralisation may become part of the answer

Interestingly, some solutions may emerge outside the traditional centralised grid structure.

Decentralised renewable systems, particularly in rural regions, are increasingly supporting local livelihoods and reducing dependence on fragile central networks. Women-led decentralised energy enterprises in parts of rural India are already demonstrating how distributed systems can improve local resilience and economic participation.

At the same time, India’s push towards electric mobility, digital infrastructure, AI-linked data centres, and industrial electrification could make electricity demand even more volatile in the coming years.

That means the country’s power market may become increasingly dynamic, financially sensitive, and technologically complex.

The irony is that India’s renewable success itself is helping create these new pressures.

The country has spent years worrying about electricity scarcity. It is now entering an era where managing abundance may become equally difficult.