A solar panel may be the most visible symbol of India’s clean-energy transition, but some of the most important battles shaping the sector’s future are unfolding far from solar parks and rooftop installations.

They are unfolding within factories that produce solar glass, wafers, ingots, cells, and other upstream components, which rarely attract public attention yet determine who captures value from the global renewable-energy economy.

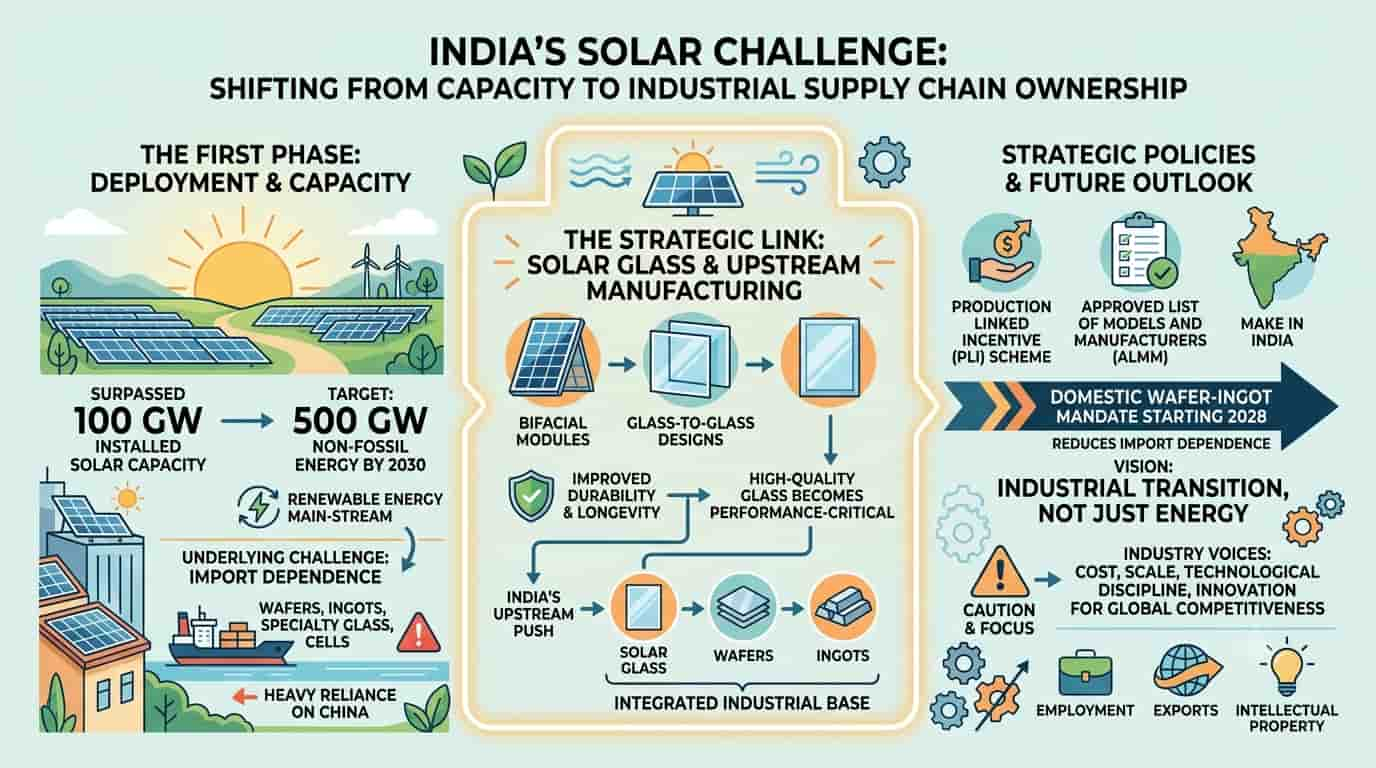

For much of the past decade, India’s solar story was defined by capacity additions. Solar parks expanded across Rajasthan and Gujarat, rooftop installations spread across cities, and renewable targets grew increasingly ambitious. Yet as India’s solar market matured, another question emerged: could the country build the industrial ecosystem to support the transition, or would it remain dependent on imported components even as renewable installations surged?

Solar glass is now becoming part of that larger strategic conversation.

The first phase was about deployment

India’s renewable-energy growth over the past decade has been remarkable.

According to the Ministry of New and Renewable Energy (MNRE), the country has committed to achieving 500 GW of non-fossil-fuel electricity capacity by 2030. Solar power is expected to account for a substantial share of this expansion.

India has already surpassed 100 GW of installed solar capacity and recently became the world’s second-largest contributor to annual solar-capacity additions, reflecting the scale and pace of deployment underway.

The first phase of India’s solar transition focused largely on building capacity, reducing tariffs, attracting investment, and accelerating project execution. That strategy helped make solar power mainstream. However, it also revealed an uncomfortable reality. Much of the value chain supporting the sector remained concentrated outside India.

For years, domestic manufacturing struggled to keep pace with deployment growth. India continued to depend heavily on imports of wafers, ingots, polysilicon, solar cells, specialty glass, and other critical inputs.

“The conversation is gradually shifting from installation numbers to supply-chain ownership,” observed a renewable-manufacturing analyst. “The next stage is not just about how much solar India installs, but about how much of the ecosystem it controls.”

Why solar glass is emerging from the shadows

Solar glass has traditionally been considered a supporting material in photovoltaic module manufacturing. Its function appears straightforward: to protect solar cells while allowing maximum sunlight transmission. Yet modern solar technologies are changing their importance.

The growing adoption of bifacial solar modules, which generate electricity from both sides, and of glass-to-glass module designs, which offer improved durability and longevity, is driving demand for higher-quality solar glass.

What was once considered a peripheral component is increasingly performance-critical. Industry participants note that improvements in module efficiency, durability, and operating life increasingly depend on advances in materials, including solar glass.

What was once considered a peripheral component is increasingly performance-critical. Industry participants note that improvements in module efficiency, durability, and operating life increasingly depend on advances in materials, including solar glass.

“As module technologies evolve, solar glass is becoming increasingly important from both a performance and a supply-chain perspective,” noted a consultant associated with renewable-manufacturing projects. “The sector is moving beyond simple assembly economics.”

The implications extend beyond technology. They raise questions of industrial resilience and strategic manufacturing capability.

China factor is reshaping global thinking

The solar industry’s supply chains remain among the world’s most concentrated. China dominates large shares of global solar manufacturing, including polysilicon, wafers, cells, and several upstream materials. That concentration has prompted governments across North America, Europe, and Asia to rethink renewable-energy supply-chain structures.

The United States of America has used the Inflation Reduction Act to promote domestic clean-energy manufacturing. Europe has emphasised industrial resilience as part of its renewable strategy. India is pursuing its own version of supply chain localisation through policy interventions and manufacturing incentives. The concern is not renewable energy itself but the excessive concentration of supply chains in a handful of geographies.

Manufacturing ambitions extend beyond modules

The growing focus on solar glass reflects a broader transformation within India’s renewable-industrial strategy.

Government initiatives such as the Production Linked Incentive (PLI) scheme, the Approved List of Models and Manufacturers (ALMM), and the Make in India initiative seek to strengthen domestic capabilities across multiple layers of the solar value chain.

The push is no longer confined to module assembly. Gradually, policymakers are focusing on upstream manufacturing.

India recently announced plans to mandate the use of domestically produced solar ingots and wafers in clean energy projects starting in 2028, underscoring the government’s aim to strengthen local manufacturing capabilities and reduce dependence on imports.

Industry investments are starting to reflect this shift. Companies such as Borosil Renewables have announced plans to expand solar glass capacity.

According to industry estimates, India’s demand for solar glass is expected to rise steadily as utility-scale solar projects expand and bifacial modules gain wider acceptance. Although domestic manufacturing capacity has grown in recent years, a significant share of the market has historically relied on imports, particularly from China.

Industry observers note that closing this gap could strengthen supply chain resilience and support a more integrated clean energy manufacturing base.

Meanwhile, companies such as Tata Power are exploring investments in domestic wafer and ingot manufacturing to strengthen India's upstream solar ecosystem. The objective is not merely to pursue import substitution. It is the creation of a more integrated industrial base capable of competing globally.

Scale alone will not be enough

Despite the opportunity, solar glass manufacturing poses significant challenges. Glass production is energy- and capital-intensive and technologically demanding. Maintaining optical quality, durability, and manufacturing consistency requires substantial investment and operational expertise.

Industry observers caution that localisation alone does not guarantee competitiveness. Manufacturers must ultimately compete on cost, technology, quality, reliability, and export potential.

“There is often an assumption that localisation automatically confers competitiveness,” said an economist tracking clean-technology supply chains. “In reality, scale, process discipline, innovation, and operational efficiency matter just as much.”

The sector must also contend with broader industry risks, including oversupply cycles, pricing pressures, technology transitions, and shifting trade dynamics.

India’s renewable sector is already beginning to encounter some of these challenges. The government has recently urged caution against excessive expansion in standalone solar module manufacturing, citing concerns about future oversupply and the need to place greater emphasis on integrated manufacturing capabilities.

That lesson applies equally to upstream segments such as solar glass.

Renewable manufacturing is the next frontier

The significance of solar glass lies not merely in the product itself but in what it symbolises. The early phase of India’s solar journey was largely an energy story. The next phase is steadily becoming an industrial narrative.

Countries are no longer competing solely to install renewable-energy capacity. They are competing to secure manufacturing ecosystems that generate technology, employment, exports, intellectual property, and long-term economic value.

The battle is gradually shifting from solar parks to the supply chain.

Solar glass may seem like a niche manufacturing segment. Yet its growing importance reflects a broader reality confronting India’s renewable ambition.

The future of the country’s clean-energy transition may depend not only on how much power it generates but also on how much of the value chain it retains within its borders.

In that sense, solar glass is more than a specialised industrial product.

It offers a window into the next chapter of India’s renewable transformation—one where industrial capability may prove as important as energy generation itself.

Follow us on : X | LinkedIn | Facebook | Bluesky