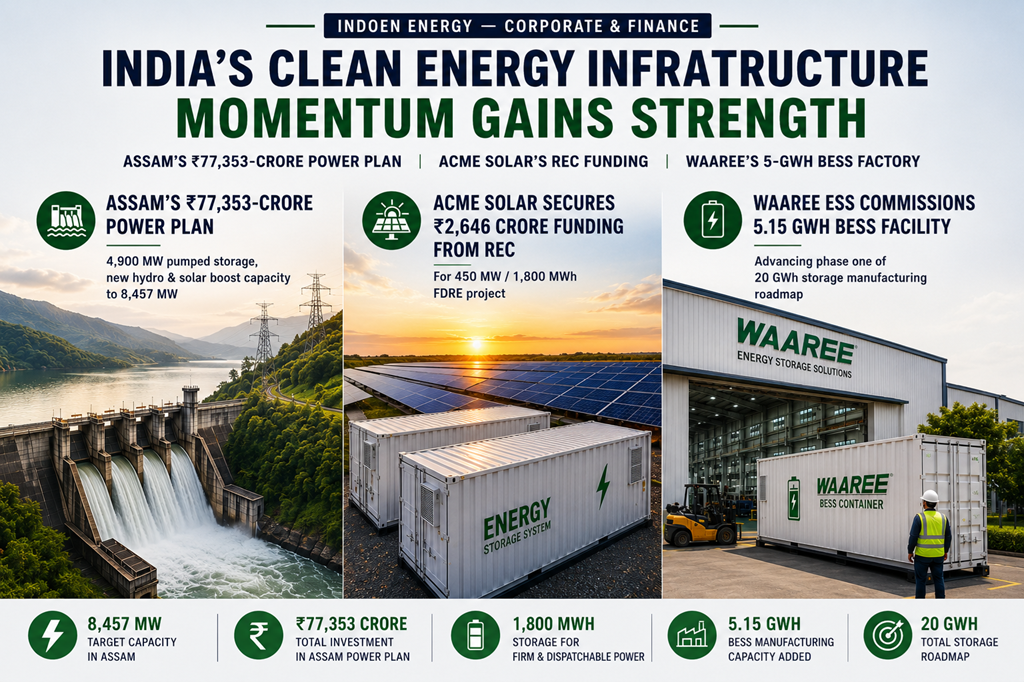

Natural gas has long occupied an awkward position in India's energy story: promoted as a bridge fuel between a coal-dominated present and a clean-energy future, yet chronically sidelined by price disadvantages, infrastructure gaps, and a regulatory environment that frustrates competition.

That tension is now sharper than at any point in recent memory.

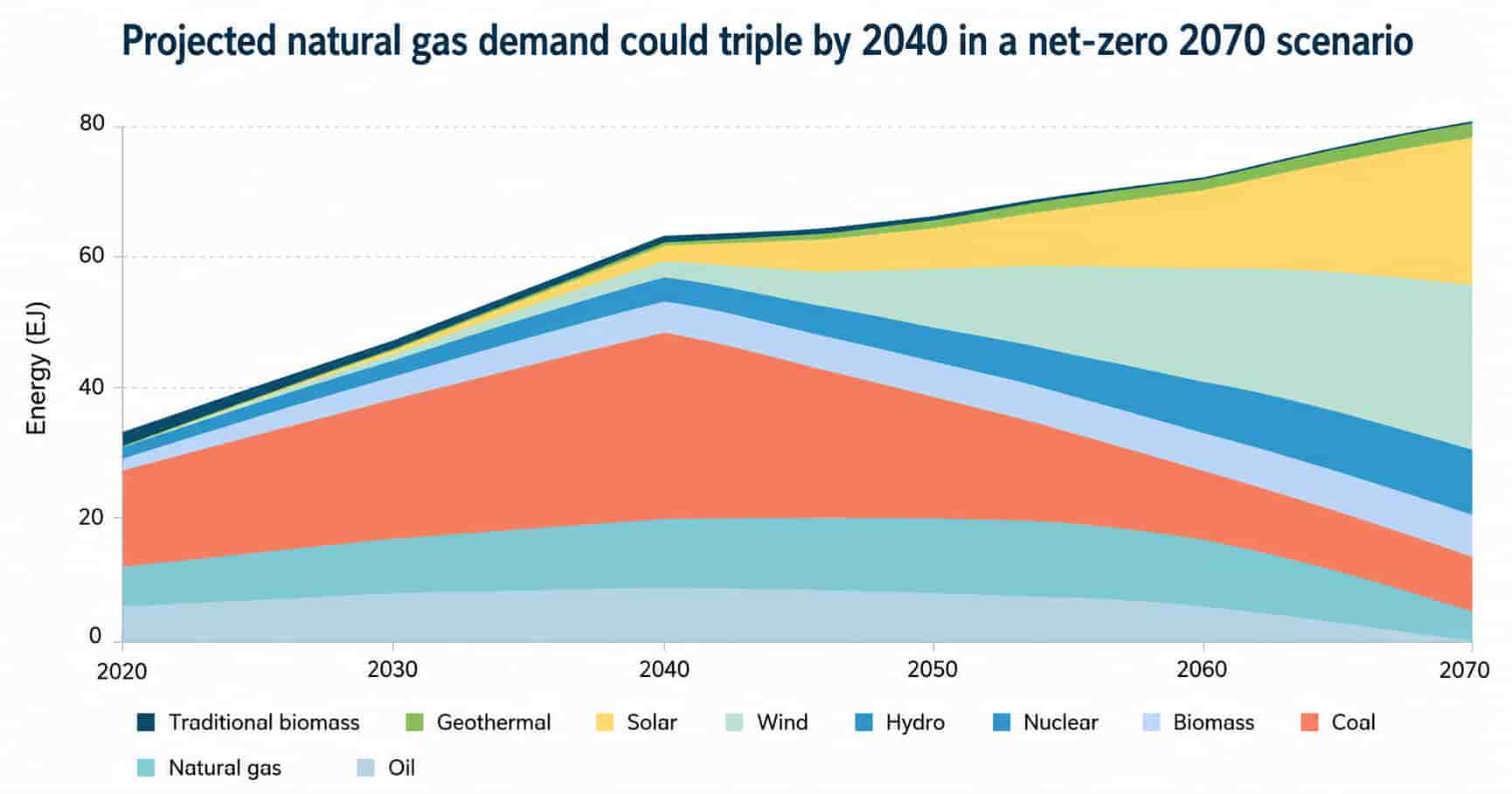

India's total primary energy demand has doubled over two decades. Coal and oil together account for more than 80% of supply. Natural gas, despite also doubling in absolute terms over the same period, holds a share of only about 5% of the primary energy mix as of 2022 — well behind the government's stated target of 15% by 2030.

Modelling by CEEW suggests that target is unlikely to be met: under a net-zero 2070 scenario, gas peaks at around 10% of the mix by 2055, then falls away. What the data do confirm is that gas demand could triple from roughly 53 billion cubic metres (bcm) to 180 bcm between 2025 and 2040 — a window that, if properly managed, could meaningfully shift India's industrial emission profile.

A supply side hobbled by stagnation

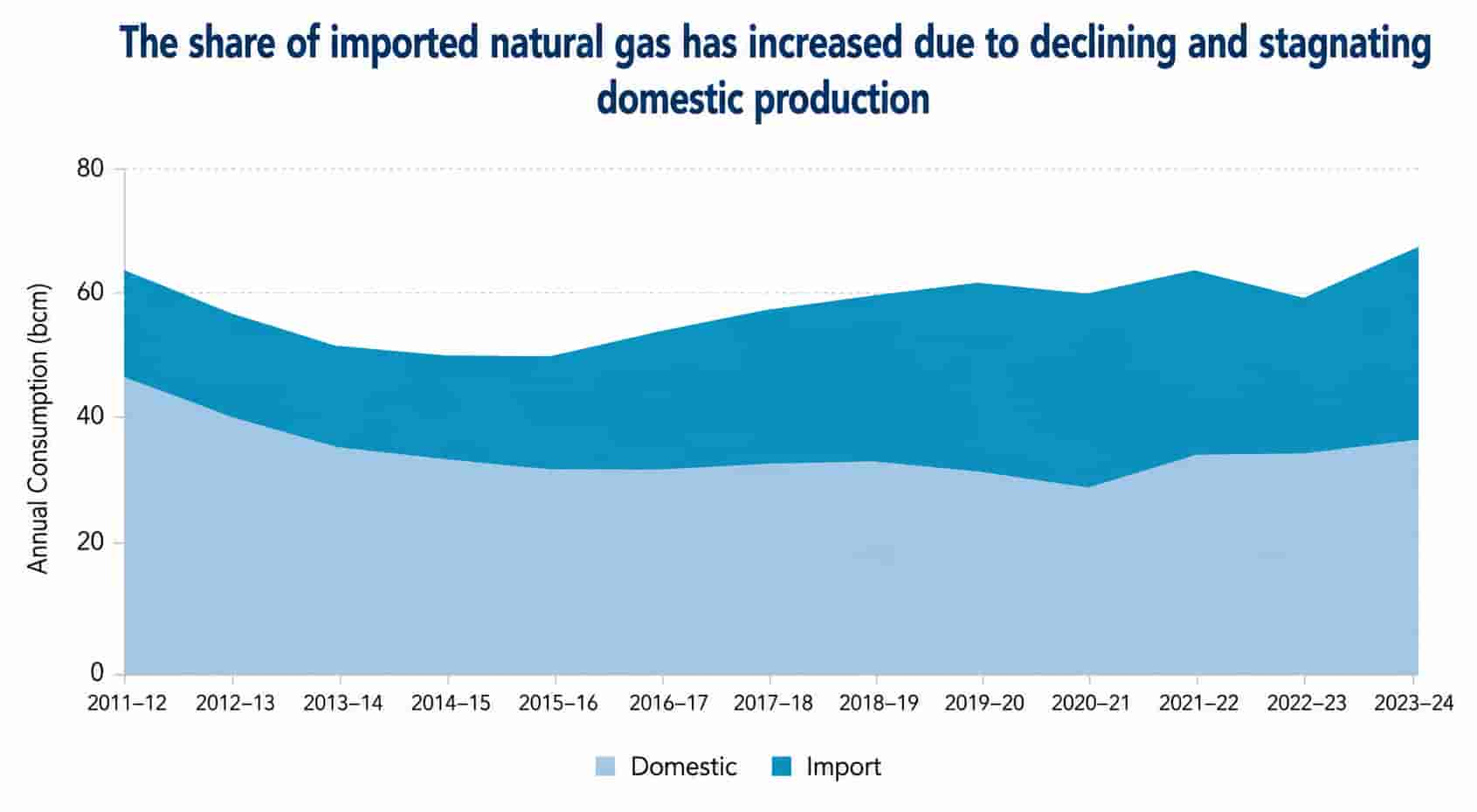

In 2023–24, India consumed a record 68 bcm of gas, of which 47% arrived as imported LNG. Domestic output has stagnated at around 36 bcm per year, constrained by difficulties in extracting gas from the Krishna–Godavari basin and declining volumes from older offshore wells. The result is an import burden of US$13.4 billion — and a supply chain concentrated to an uncomfortable degree.

Qatar accounts for 40–50 % of India's LNG imports. That dependence was exposed brutally in early 2026, when the conflict in West Asia effectively closed the Strait of Hormuz and disrupted nearly 60% of India's LNG flows, forcing emergency redirection to priority sectors. The episode has accelerated calls, documented in the joint CEEW–Hoover Institution policy brief published this month, for urgent supplier diversification.

The structural opportunity to diversify exists. The United States is expected to add over 100 million tonnes per annum (Mtpa) of new liquefaction capacity by 2030, more than doubling its 2024 base, while the UAE is set to nearly triple its own.

Canada, Mozambique, Argentina and Australia are adding further volumes. Since December 2024, Indian importers have already signed four long-term contracts totalling 11 Mtpa linked to Henry Hub prices. In 2023–24, US LNG was 25% cheaper than the quantity-weighted average from other suppliers — US$8.3 per million British thermal units against US$11.1/MBtu.

“The window to lock in competitive long-term contracts is now, while exporting countries are still in a build-out phase and keen to secure demand visibility,” a senior analyst at an energy policy research institution noted. “India's leverage as a major buyer will diminish once the global supply wave tightens.”

Sectors with the most to gain

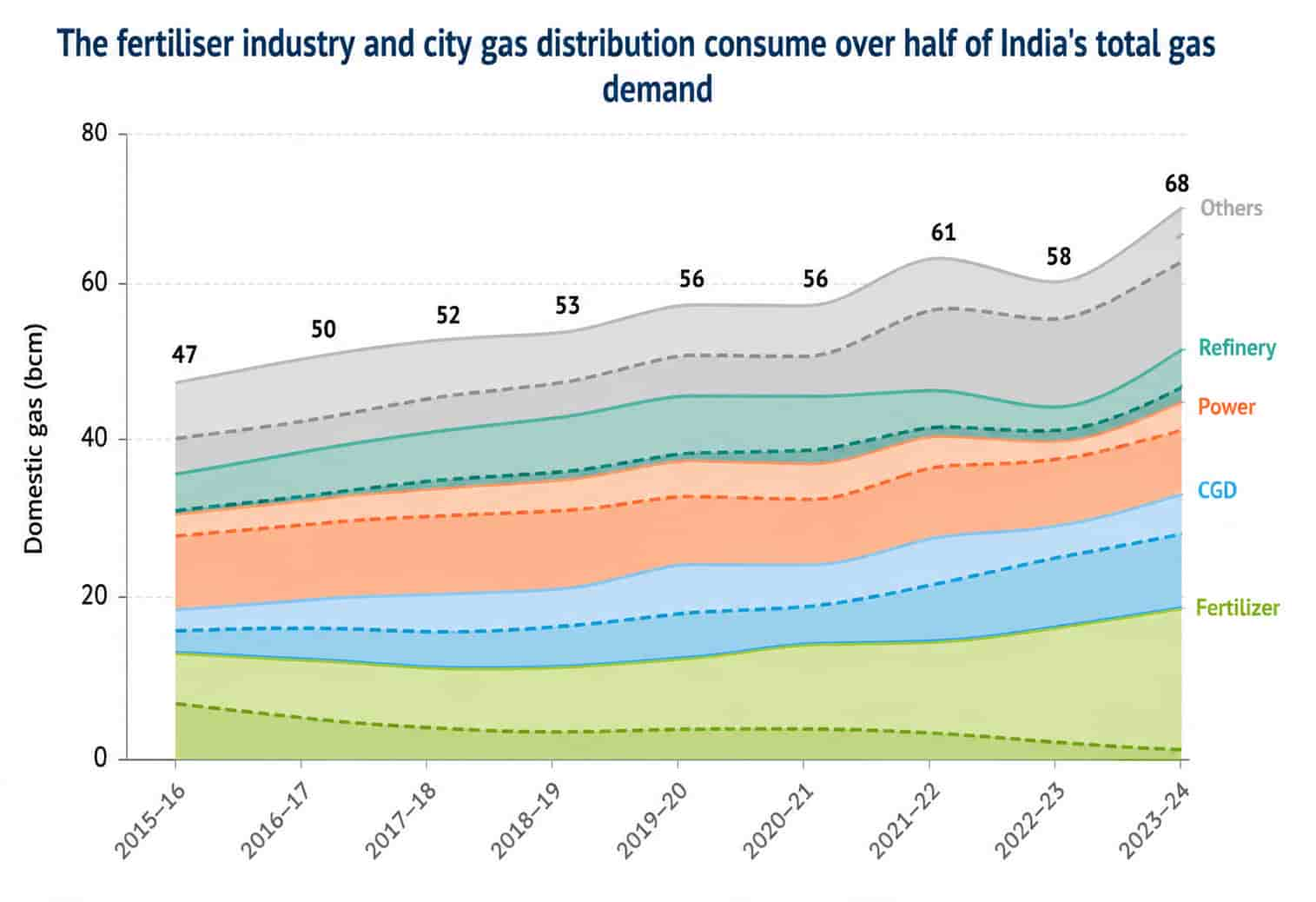

Demand growth will not be evenly spread. The fertiliser sector absorbs more than 30% of India's gas, with all urea plants entirely dependent on it as a feedstock.

Annual fertiliser subsidies exceed US$20 billion, making affordable gas supply a direct fiscal matter. But the National Green Hydrogen Mission is progressively redirecting these anchor sectors toward green hydrogen — meaning incremental gas demand here is likely to plateau rather than surge.

The more consequential opportunity lies in steel and transport. India's steel industry is the second largest in the world yet emits 2.36 tonnes of CO₂ per tonne of crude steel against a global average of 1.91 tonnes, a gap driven by roughly 90% reliance on coal.

Gas-based steelmaking cuts emissions by more than 30% over coking coal routes and up to 60% when paired with renewable electricity. Crucially, the same infrastructure can subsequently run on green hydrogen without major modification — making it genuinely future-proof. With India targeting 300 Mtpa of steel capacity by 2030, even 24 Mtpa of gas-based output could generate additional annual demand of around 7.3 bcm.

In heavy-duty transport, LNG offers a medium-term pathway to decarbonise long-distance freight while electric and hydrogen trucks remain commercially unready at scale.

Combined EV and LNG adoption represents the strongest near-term scenario for moderating diesel demand growth, which the report finds would otherwise continue rising until 2047 without alternative fuel interventions.

Power plants idling, pipes pointing the wrong way

Over 25 gigawatts of gas-based power capacity recorded a plant load factor of only 14.9% in 2023–24. Gas-fired power costs ₹7.2 per kilowatt-hour (US$76.19 for 1,000 kilowatt-hour) against ₹4.6/kWh (US$48.68 for 1,000 kilowatt-hour) for coal and under ₹4/kWh (US$42.33 for 1,000 kilowatt-hour) for solar and wind, making routine baseload use economically indefensible. Yet these plants are uniquely suited to grid balancing: they ramp up and down far faster than coal plants and were deployed precisely for this purpose during record heatwaves in 2024.

The obstacle is pipeline architecture. Capacity booking is operator-specific and uses a point-to-point tariff structure that prevents flexible or round-the-clock bookings. Transitioning to an entry–exit model — under which consumers book independent injection and withdrawal rights across the network — would bring India closer to the architecture of mature gas markets in the EU and the UK, and materially improve liquidity.

Taxation compounds the problem. Natural gas remains under the value-added tax regime despite constitutional eligibility for the goods and services tax (GST). State VAT rates range from zero in Delhi to 25% in Chhattisgarh, with no input tax credit, creating cascading cost burdens along the supply chain.

In 2023–24, central public sector enterprises paid over ₹2,50,000 crore (US$26.5 billion) in total state sales taxes and VAT, of which only ₹15,633 crore (US$1.7 billion) related to crude oil and natural gas — a relatively modest revenue base that should, in principle, make consensus on GST inclusion achievable.

The methane caveat

Any honest accounting of gas's role must confront methane. According to the US Environmental Protection Agency, 60% of supply-chain methane emissions occur at the production stage alone.

Methane carries a 20-year global warming potential roughly 83 times that of CO₂, meaning uncontrolled leakage can rapidly erode gas's emission advantage over coal. India currently lacks standardised methane measurement and control protocols for its gas supply chain.

“Without credible methane protocols, the claim that gas is a climate-aligned bridge fuel rests on an assumption we cannot yet verify,” said an analyst at a climate and energy research institution. “Monitoring infrastructure is the price of the policy credibility that makes gas expansion politically sustainable.”

Indoen Energy has previously examined a related dimension of this fragility in its analysis of whether India is entering an era of energy demand destruction, noting that LNG imports fell sharply during a period of price volatility — evidence that industrial consumers remain acutely price-sensitive.

The broader conclusion of the brief is unambiguous: unlocking India's gas economy is not a single-lever problem. It requires recalibrating an overambitious national target, consolidating demand signals to strengthen import contract negotiations, bringing gas under GST, reforming pipeline access architecture, diversifying away from Qatar before the 2030 capacity wave subsides, and establishing methane controls that give the fuel the environmental credibility its economic case requires. Without that combination, the 15% ambition risks remaining exactly what it has been for a decade — a headline with no mechanism behind it.

Follow us on : X | LinkedIn | Facebook | Bluesky