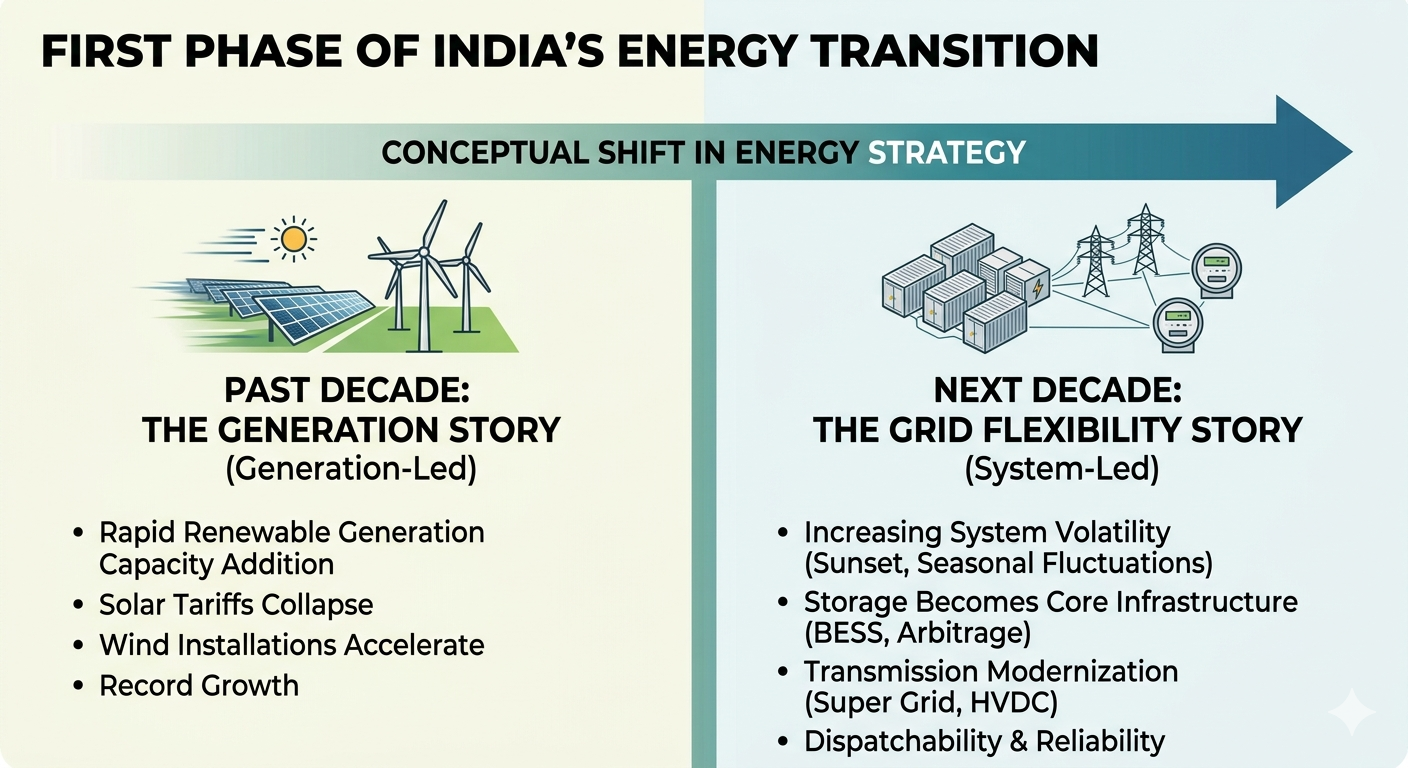

India’s clean-energy transition is entering a more complex and capital-intensive phase. For nearly a decade, the country’s energy strategy revolved around adding renewable generation capacity at record speed. Solar tariffs collapsed, wind installations accelerated, and ambitious national targets helped position India among the world’s fastest-growing renewable energy markets.

But a growing body of evidence now suggests that India’s next major energy challenge may no longer be producing electricity. Instead, it is rapidly becoming about storing, balancing, moving, and monetising that electricity across an increasingly volatile and decentralised grid.

A wave of recent developments — from large standalone battery energy storage system (BESS) projects and aggressive storage auctions to plans for a China-style super grid and rising concerns over project profitability — indicates that India’s energy transition is shifting from a generation story to a grid flexibility story.

The implications could reshape the economics of the country’s power sector over the next decade.

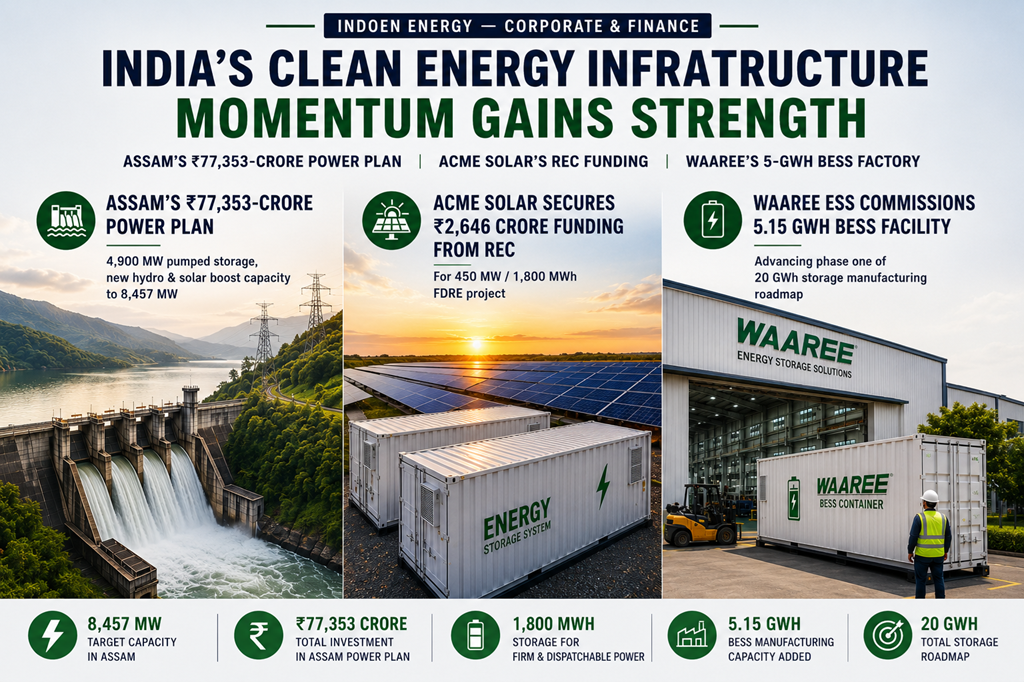

India recently commissioned one of its largest standalone battery storage facilities, underscoring how storage is beginning to move from pilot-scale deployment towards system-level infrastructure. At the same time, the government is discussing faster BESS rollout and transmission expansion to support renewable integration, while developers continue to aggressively bid for storage-linked projects despite growing industry concerns about long-term viability.

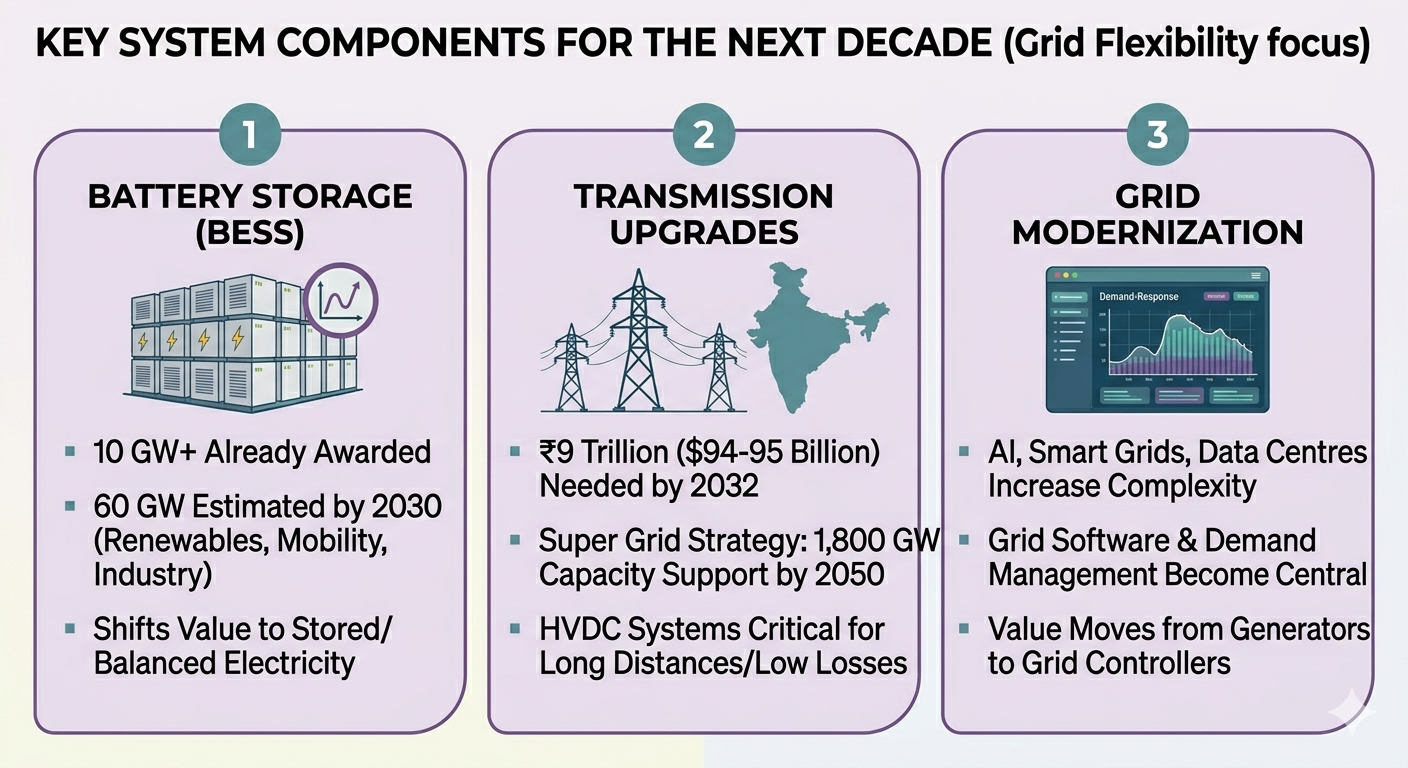

India has already awarded more than 10 GW of battery storage capacity through auctions, according to industry estimates, while policymakers and analysts believe the country could require around 60 GW of storage capacity by 2030 to support renewables, electric mobility, and emerging industrial demand.

More importantly, large projects are increasingly moving from tender announcements to operational execution.

The pace of deployment is also accelerating on the ground. Chinese power electronics firm Kehua recently announced the grid connection of a 180 MW/360 MWh standalone energy storage project in India, one of the larger operational battery-storage installations currently visible in the market.

The project highlights how utility-scale standalone storage is gradually moving beyond pilot deployment towards commercially integrated grid infrastructure.

The scale of the infrastructure challenge is becoming increasingly clear. A recent industry assessment cited by The Economic Times estimated that India’s power transmission sector alone could witness nearly ₹9 trillion ($94-95 billion) in investments by 2032 as the country expands renewable energy capacity and modernises its electricity network.

The broader transition towards flexibility-led electricity systems has already been explored in earlier Indoen Energy coverage on round-the-clock renewable systems.

The transition after the transition

The larger shift underway is subtle but profound.

For years, renewable energy policy discussions focused primarily on capacity additions. India’s solar and wind sectors benefited from falling equipment costs, strong policy signalling, and large-scale auctions. The challenge was viewed largely as one of generation.

That assumption is beginning to break down.

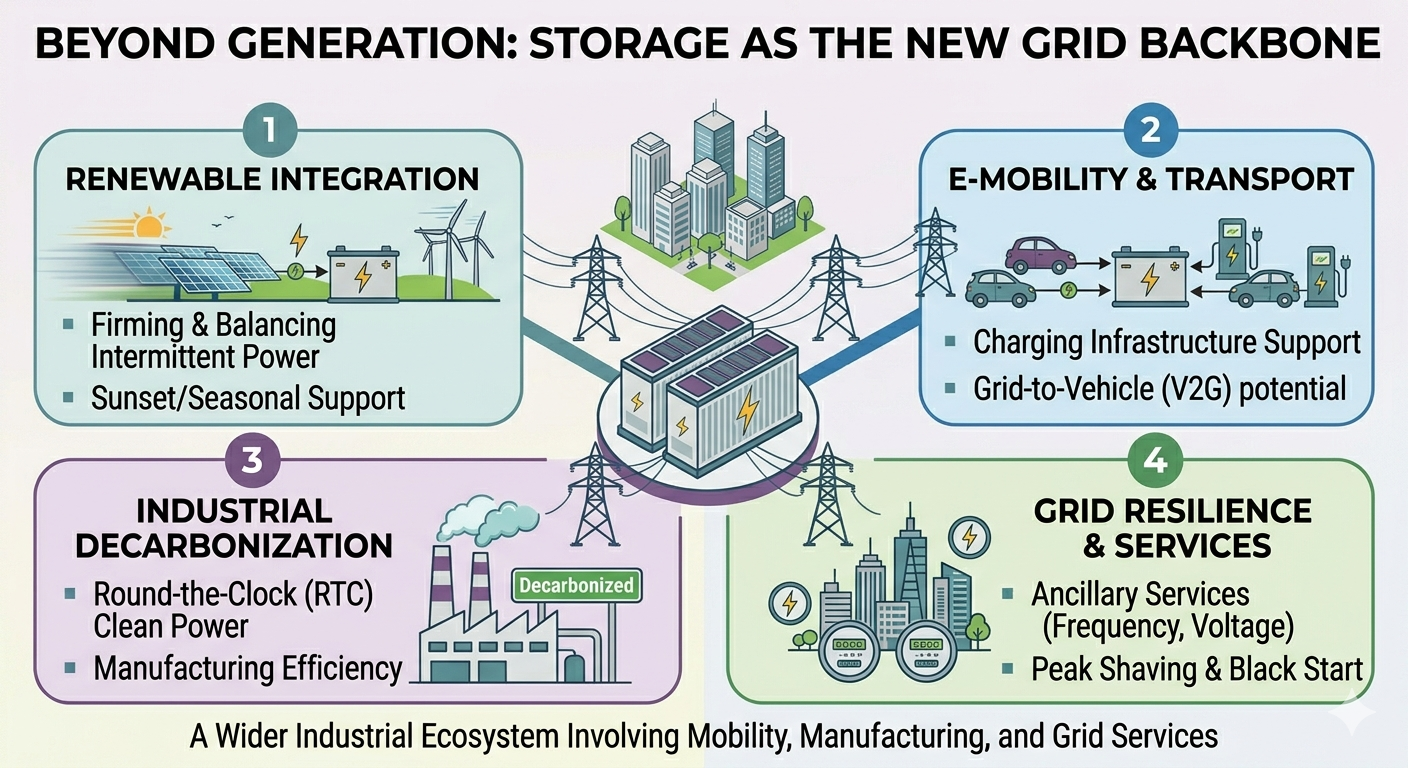

As renewable penetration rises, electricity systems become more unstable and unpredictable. Solar output falls sharply after sunset. Wind generation fluctuates seasonally. Heatwaves create sudden spikes in cooling demand. Electric vehicle charging networks, industrial electrification and AI-linked data centres are expected to increase volatility further.

India’s proposed “super grid” strategy reflects this emerging reality. The idea is to create large transmission corridors capable of moving renewable electricity across regions at scale, similar to transmission systems being developed in China.

The numbers involved are staggering. India is reportedly exploring transmission systems capable of supporting as much as 1,800 GW of renewable energy capacity by 2050. According to the media reports, India could add around 470 GW of additional renewable-energy capacity by 2032 alone, requiring massive expansion of long-distance power evacuation infrastructure and high-voltage transmission corridors.

This is also accelerating interest in High-Voltage Direct Current (HVDC) systems, which are increasingly viewed as critical for transporting renewable electricity across large distances with lower transmission losses. Industry estimates cited in the report suggest the global HVDC market could grow from around US$15 billion to over US$31 billion by 2035 as countries build larger renewable-energy corridors.

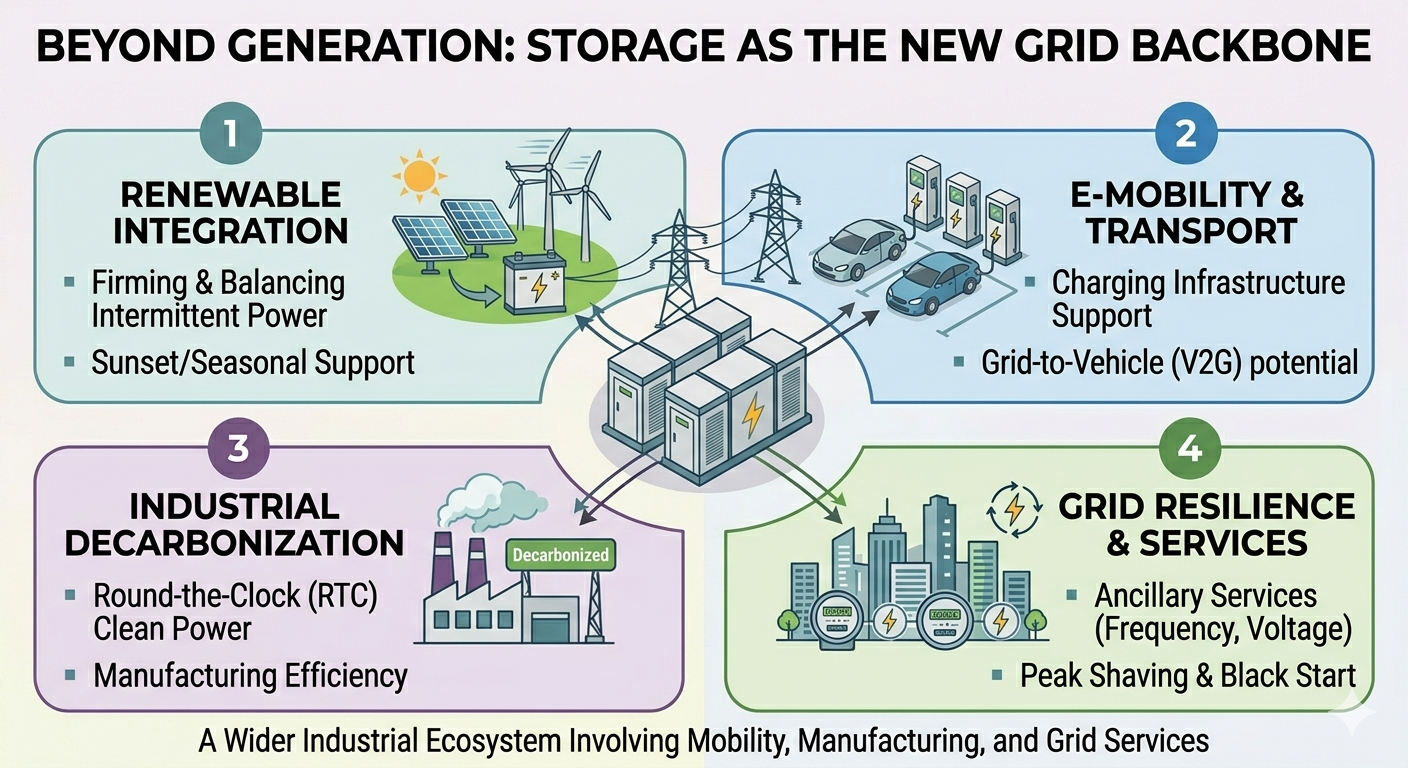

The shift also explains why storage is no longer being treated as a supporting technology. Increasingly, it is becoming core infrastructure.

In many future scenarios, the value of electricity may depend less on who generates power and more on who can store, balance, and dispatch it at the right time.

A new profitability problem emerges

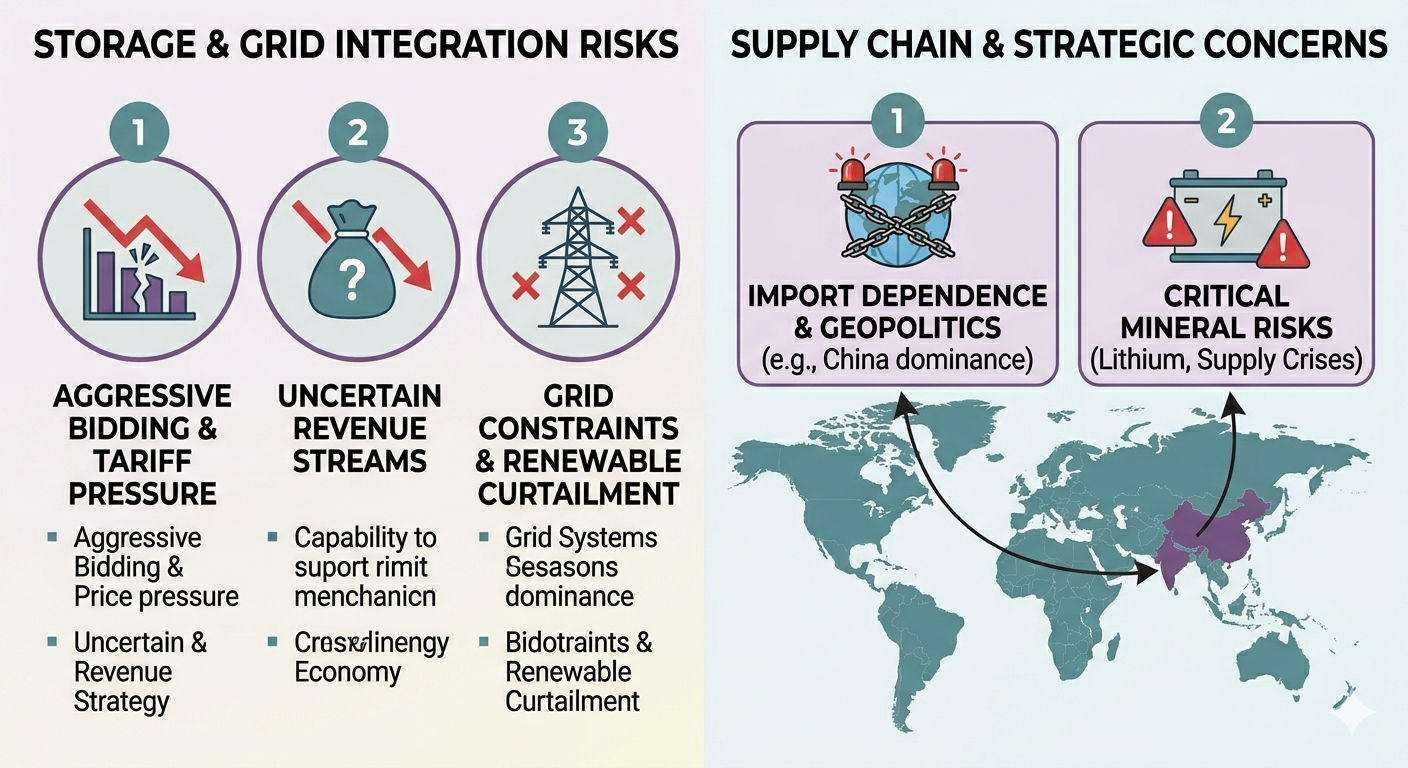

Yet beneath the optimism surrounding storage growth, financial concerns are quietly intensifying.

Several industry reports now warn that India could be recreating some of the structural problems seen during the early solar boom. Aggressive bidding, falling tariffs, uncertain revenue streams, and intense competitive pressure are beginning to raise questions about long-term profitability.

The challenge is that battery storage economics remain heavily dependent on policy design, utilisation rates, ancillary-service markets, and electricity price volatility.

Unlike solar plants, which generate predictable daytime electricity, storage projects often rely on complex revenue models involving grid balancing, peak shaving, frequency regulation, and electricity arbitrage. These markets are still evolving in India.

Some industry executives privately worry that developers may be underestimating future operational risks in the rush to secure market share.

The concern is not theoretical. Several international markets, including parts of Europe and Australia, have already experienced extreme pricing volatility linked to renewable integration and storage economics.

India is already beginning to witness some of these stresses. Renewable curtailment and transmission bottlenecks are emerging in certain regions as solar generation grows faster than evacuation infrastructure. Reports of clean electricity being wasted because of grid constraints are reinforcing concerns that transmission upgrades may struggle to keep pace with renewable deployment.

At the same time, battery prices remain exposed to supply-chain risks involving lithium, critical minerals, and geopolitics.

Storage is becoming geopolitical

Another underexplored dimension of India’s storage push is its geopolitical significance.

China currently dominates much of the global lithium-ion battery supply chain, from refining and processing to manufacturing capacity. India’s attempt to rapidly scale domestic storage deployment therefore intersects with broader concerns around industrial security, import dependence, and strategic autonomy.

This partly explains why Indian automakers and industrial groups are accelerating investments in battery manufacturing and EV-linked storage ecosystems.

The shift is also beginning to attract a broader range of industrial players.

A growing number of Indian industrial and manufacturing companies are also beginning to position themselves around the emerging storage economy.

Railway and mobility-focused manufacturer Jupiter Wagons recently announced battery energy storage agreements worth 110 MWh through its energy subsidiary, signalling how companies outside the traditional power sector are increasingly viewing storage infrastructure as a long-term growth opportunity.

The development reflects how battery storage is evolving into a wider industrial ecosystem involving mobility, manufacturing, power electronics and grid services.

The geopolitical implications of future electricity systems and energy infrastructure were also touched upon in an earlier Indoen Energy analysis on global power politics and electricity systems.

Countries capable of controlling future electricity flexibility infrastructure — including batteries, smart grids, power electronics, HVDC systems and transmission networks — could gain major advantages in manufacturing, AI infrastructure, and energy-intensive industries.

The global energy equation is changing

India’s evolving storage strategy also mirrors broader global energy trends.

A recent assessment by the International Renewable Energy Agency suggested that renewable-plus-storage systems are becoming increasingly competitive with fossil-fuel-based round-the-clock electricity generation in several markets.

Meanwhile, large energy developers worldwide are rapidly scaling storage-linked projects. In Australia, for instance, Equis recently launched Greenpoint Energy with a 2.5 GW portfolio combining battery storage and wind projects.

What makes the Indian story particularly important is scale.

India is simultaneously attempting to expand renewable generation, electrify transport, modernise industrial systems, manage rising electricity demand, and maintain affordable tariffs. Power demand itself is projected to grow at a compound annual rate of around 6.4% until 2030, driven by economic growth, electrification, cooling demand, railways and digital infrastructure expansion.

Few countries have attempted such a large-scale transition under similar developmental and financial constraints.

The next phase of India’s energy transition

The emerging reality is that India’s energy transition is becoming less about installing solar panels and more about redesigning the electricity system itself.

Storage, transmission, grid software, balancing services, and demand management are likely to become increasingly central to the future power economy.

This could also reshape investment patterns across the sector.

The next generation of energy winners may not necessarily be companies producing the cheapest electricity. Instead, they may be firms capable of managing flexibility, reliability, dispatchability and power evacuation at scale.

That marks a major conceptual shift in how the energy transition is understood.

It also means the future battleground of India’s power sector may increasingly revolve around who controls the grid — not merely who generates electricity.