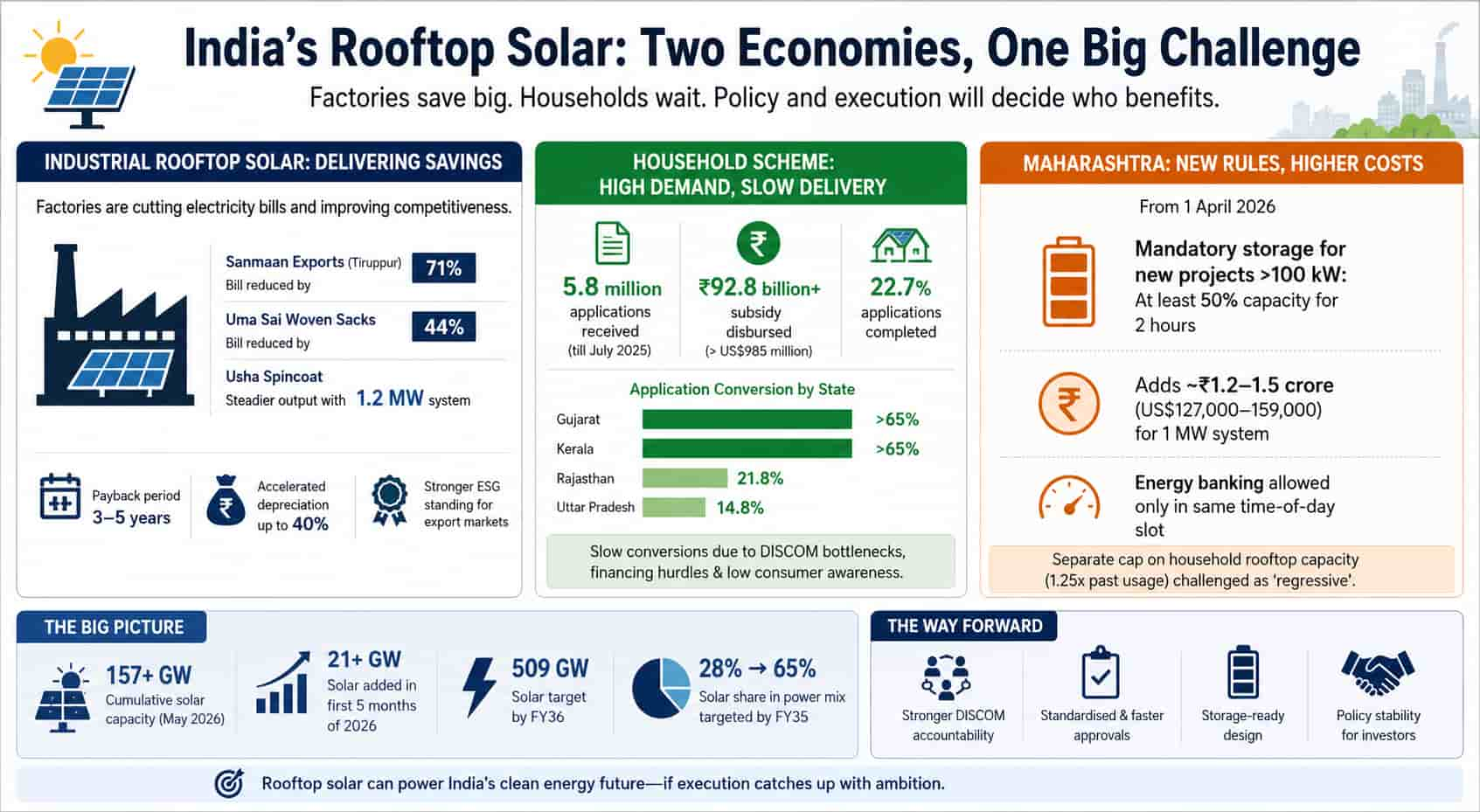

India's rooftop solar revolution is fracturing into two very different stories. Textile factories from Tiruppur to Coimbatore are slashing electricity bills using the same panels that, under the government's flagship US$7.95 billion household scheme, are taking years to reach rooftops in several large states.

Gujarat and Kerala are converting most applications into working systems; Uttar Pradesh and Rajasthan are not. Maharashtra has just made the industrial side costlier too.

For years, the pitch behind India's rooftop solar push was straightforward: cheap panels, falling costs, and a government cheque to bridge the gap. That pitch is now colliding with the messier business of delivery.

The factories making it work

Inside textile units in Tiruppur, Coimbatore and Surat, the economics of rooftop solar are no longer theoretical. Tata Power says Sanmaan Exports has cut its electricity bill by nearly 71% after switching to solar, Uma Sai Woven Sacks has reduced power costs by roughly 44%, and Usha Spincoat reports steadier output since installing a 1.2 MW system.

These are not trivial numbers for an industry contributing more than 2.3% of India's GDP and employing over 45 million people, often on thin margins.

Bill cuts of 30 to 70%, three-to-five-year payback periods and accelerated depreciation of up to 40% make rooftop solar a rare investment that pays for itself while bolstering a factory's standing with export buyers enforcing codes such as GOTS, Oeko-Tex and the Higg Index.

The reason is simple: spinning, weaving and dyeing run continuously through daylight hours, so generation and consumption line up almost perfectly, something few other industrial loads can claim.

The households still waiting

Compare that with PM Surya Ghar: Muft Bijli Yojana, which has an approved outlay of ₹750.21 billion (US$7.95 billion) and offers households a subsidy of up to ₹78,000 (roughly US$830) towards rooftop systems. Demand has been overwhelming: by July 2025, 5.8 million applications had been filed, with subsidy disbursements already exceeding ₹92.8 billion (US$985 million).

Conversion into installed rooftops, however, has lagged badly, with only around 22.7% of applications completed, according to analysis by the Institute for Energy Economics and Financial Analysis cited in PV Tech.

The shortfall is not evenly spread. Gujarat and Kerala have converted more than 65% of applications into working systems; Rajasthan managed 21.8% and Uttar Pradesh just 14.8%, IEEFA's Gaurav Upadhyay noted in his interview, attributing the gap to stronger distribution-company engagement and consumer awareness in better-performing states.

Financing adds friction of its own: public-sector banks offer cheaper loans but slower approvals, while non-banking lenders move faster but charge more, leaving many lower-income households caught between the two.

Indoen Energy has previously examined how unevenly India's wider clean-energy boom is landing across states, grids and consumers, and the rooftop scheme's own numbers now tell much the same story at household level.

Maharashtra raises the stakes

Just as the industrial case for rooftop solar was strengthening, India's most industrialised state moved the goalposts. From 1 April 2026, Maharashtra's revised renewable energy and storage policy requires any new rooftop or open-access solar project above 100 kW to add battery storage equal to at least half its capacity, for a minimum of two hours, effectively turning every new factory rooftop project into a solar-plus-storage project by default.

For a 1 MW installation, that works out to roughly 1 MWh of battery capacity, costing ₹1.2–1.5 crore (US$127,000–US$159,000) at current prices, according to Mercom India. A separate tariff order restricting energy banking to the same time-of-day slot has further weakened returns on existing C&I solar projects in the state.

The same government has separately been pressed by the federal renewable energy ministry to roll back a rule capping new household rooftop capacity at 1.25 times a consumer's past electricity use, after officials called the move ‘regressive.’

Tata Power's own carport project elsewhere in the state shows how active Maharashtra remains in distributed clean energy, even as its regulatory signals pull in different directions.

The macro numbers still impress

None of this shows up in India's headline solar statistics. The country added more than 21 GW of solar in the first five months of 2026, taking cumulative capacity past 157 GW, ministry data reported by SolarQuarter show.

Yet May's addition of 2.81 GW was actually down 2.7% on a year earlier, even as wind installations jumped 58.5%, Saur Energy reported, a reminder that the headline growth curve is smoother than the underlying data.

Brokerage Nuvama expects solar capacity to grow at a 22% compound annual rate through 2035, driven largely by data-centre and green hydrogen demand, potentially adding 251 GW to 406 GW of new capacity and lifting solar's share of the power mix from 28% today to as much as 65% by FY35.

Indoen Energy has separately examined how this demand-led shift, rather than policy alone, is now reshaping investment across the sector.

Globally, the contrast is sharper still. An Ember analysis published this month found solar met roughly 75% of the world's electricity demand growth in 2025, while gas's share of the global power mix fell to a five-year low of 21.8%. India's own gas-fired generation peaked in 2010 at 118 terawatt-hours and has since fallen by 69 TWh, the third-largest such decline of any country after Japan and the United Kingdom.

What needs to change

The pattern emerging is one of bifurcation rather than failure.

Utility-scale solar and industrial captive demand are advancing broadly on schedule, helped by predictable daytime loads and quick payback periods. Household rooftop solar, by contrast, depends on thousands of individual distribution-company approvals, net-metering inspections and financing decisions, each a potential point of delay, and that machinery has not kept pace with application volumes.

Closing the gap will likely need less emphasis on subsidy size and more on distribution-company accountability, standardised inspection timelines and storage-ready design, precisely the issues now surfacing in Maharashtra.

With India targeting 509 GW of solar by FY36, the country can probably absorb a slower rooftop scheme. It cannot afford one that only works for half the households it was built for.