Start with the figure that ought to concern every transport planner in Delhi: 1 per cent. That is electricity's share of India's on-road transport energy mix in 2025-26, up from a mere 0.05 per cent six years earlier. Petrol still accounts for half of all transport energy, diesel for another two-fifths, and CNG has quietly grown to a tenth.

Measured in the energy actually flowing through India's vehicles rather than in headline sales figures, the electric transition has barely dented the fossil-fuel base it was meant to displace, according to an analysis published by a Down To Earth drawing on government vehicle-registration and energy-consumption data.

This is not for want of capital. An estimated ₹2.23 lakh crore (US$23.2 billion) flowed into India's electric transport ecosystem between 2020 and 2025, as per estimates cited in the same analysis. Yet the capital required to hit the government’s 2030 electrification targets is put at ₹12.5 lakh crore (US$129.8 billion) — meaning five years of investment has covered only around 18% of what the next four years will need.

That gap is the real subject of this story, and Delhi's newly notified EV Policy 2026 is the first serious attempt by any Indian state to close it through regulation rather than cheques.

Delhi swaps incentives for deadlines

Delhi swaps incentives for deadlines

Delhi’s EV Policy 2020 relied almost entirely on purchase subsidies and tax waivers, and it worked well enough to push the capital’s EV penetration in new vehicle sales to around 12-14% by 2025-26. But Policy 2026, effective from 1 July 2026 to 31 March 2030, marks a deliberate break from that model.

From 1 January 2027, only electric three-wheelers and light N1-category goods carriers can be freshly registered in the capital. From 1 April 2028, the same applies to two-wheelers. Strong hybrids, notably, are excluded from all fiscal support — a decision aimed squarely at zero tailpipe emissions rather than incremental efficiency gains.

The financial backing is substantial: roughly ₹7,000 crore (US$725 million) in direct purchase incentives and a further ₹8,000 crore (US$830 million) for infrastructure, taking the total package to around ₹15,000 crore (US$1.6 billion), alongside a target of 32,000 new public charging points across the city.

Two-wheeler buyers can claim ₹30,000 (about US$310) in year one, tapering to ₹10,000 (about US$105) by year three; auto-rickshaw buyers get ₹50,000 (about US$520) falling to ₹30,000 (about US$310). Passenger-car tax exemptions are capped at vehicles priced up to ₹30 lakh (about US$31,150) ex-showroom, and subsidised vehicles cannot be resold outside Delhi for three years — a lock-in designed to prevent buyers from gaming the scheme.

The government’s own ambition is unambiguous, per an assessment from a media report: Delhi aims for 95% of all new vehicle registrations to be electric by 2027 and for EVs to make up 30% of its total vehicle fleet by 2030, up from around 12.6% of new sales today — a target that will require the fastest sustained electrification rate attempted by any Indian city.

The policy also pairs its registration mandate with a scrappage lever aimed squarely at the capital's oldest, most polluting cars. Owners who trade in a vehicle bought before 1 April 2020 for a battery-electric replacement will receive a cash incentive of roughly ₹1 lakh (US$1,040), according to a another media report on the policy's finalisation.

That is a deliberate departure from the ‘new-purchase-only’ logic of most subsidy schemes: rather than simply rewarding EV buyers, it specifically targets the oldest and highest-emitting vehicles for removal, on the theory that scrappage delivers a faster air-quality payoff than incremental new-sales growth ever could.

Registrations are booming even as energy use barely moves

Registrations are booming even as energy use barely moves

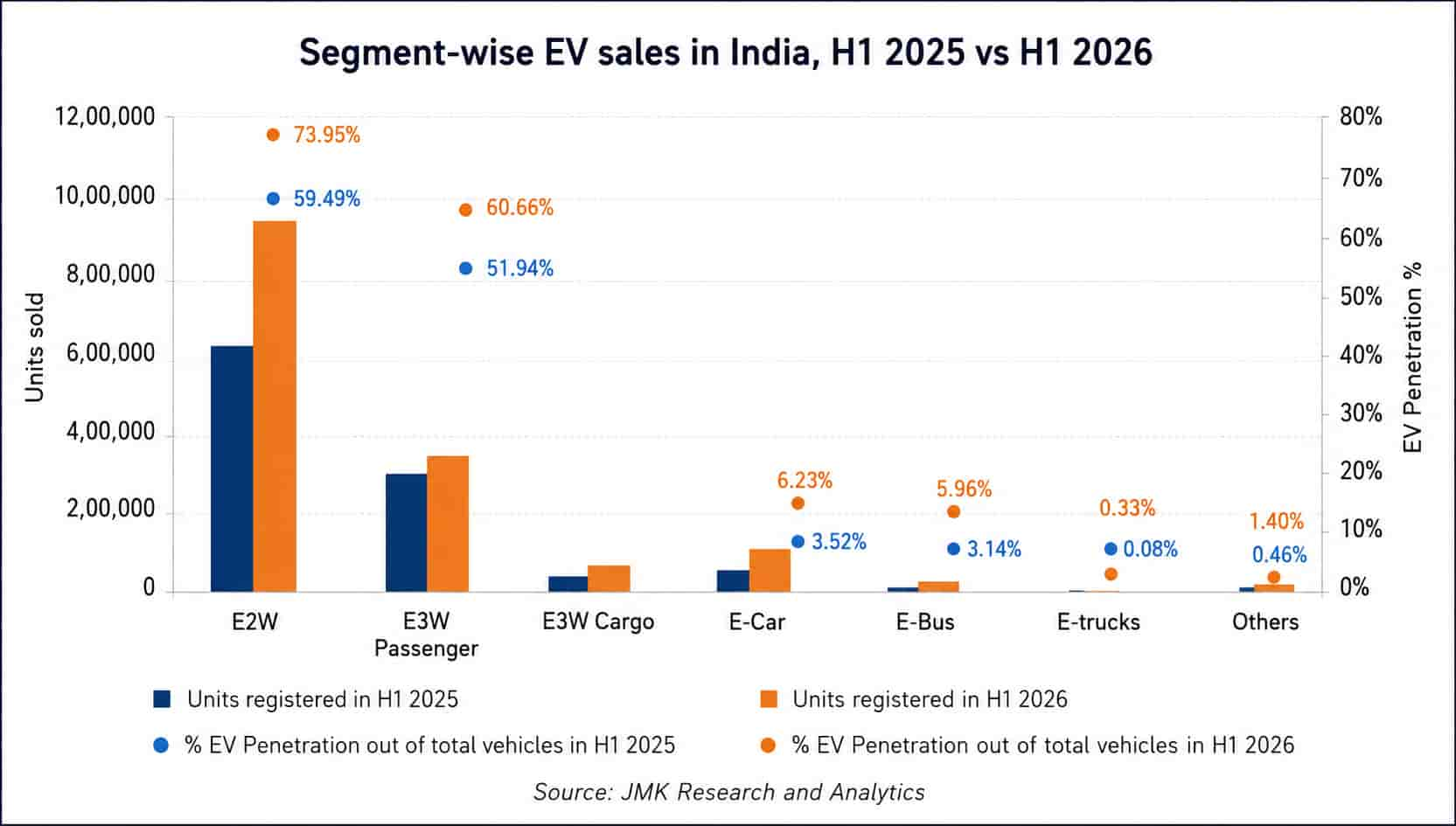

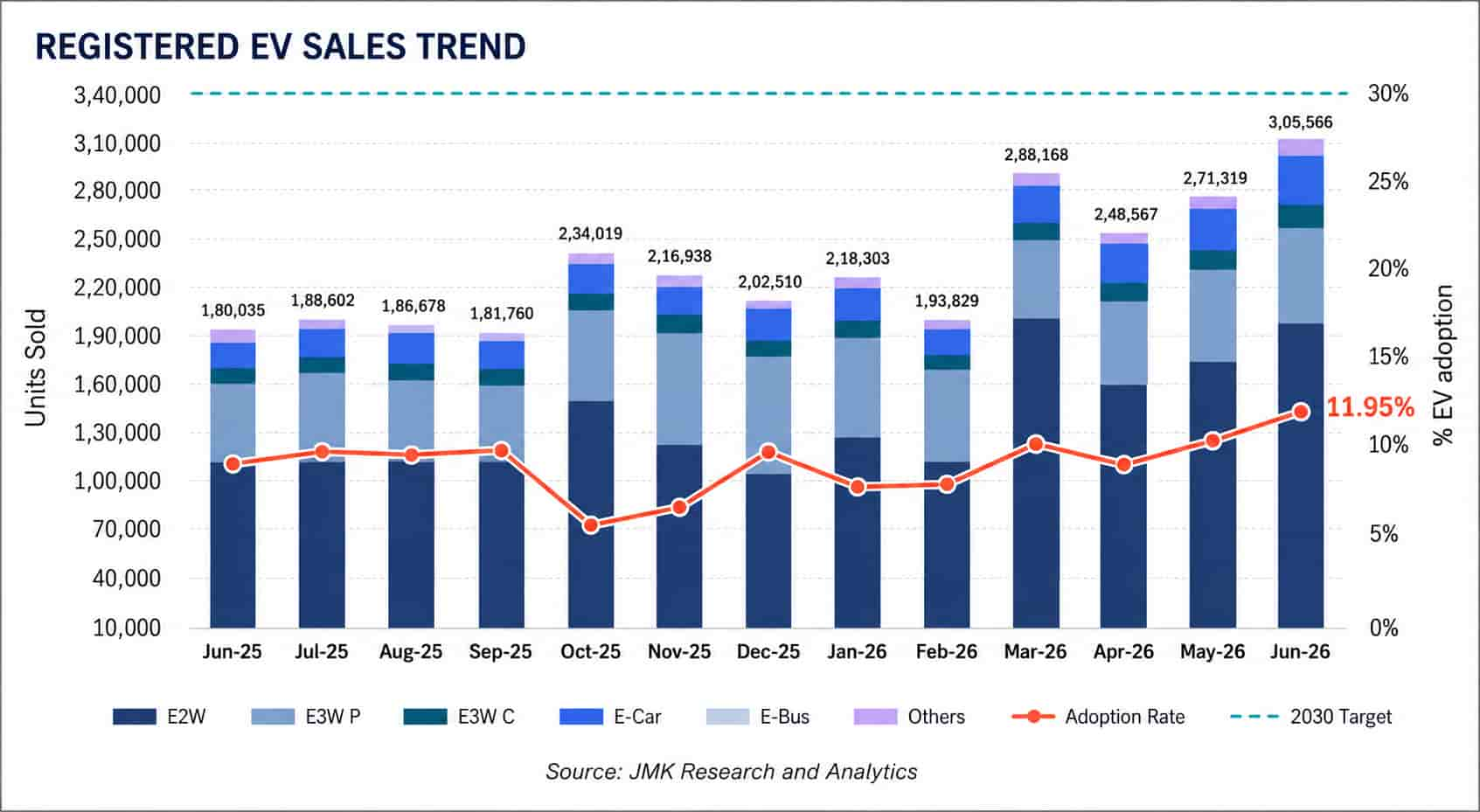

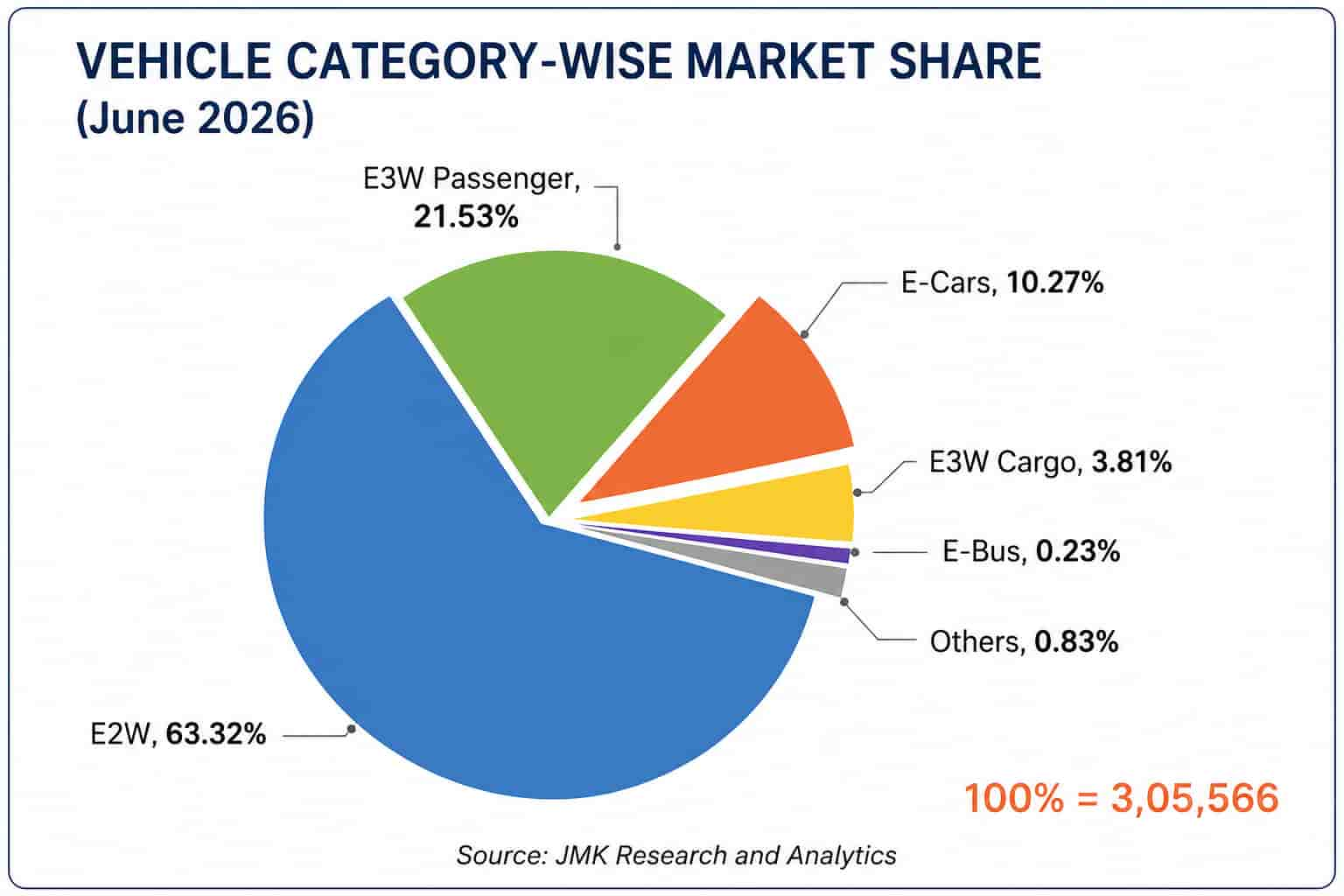

Here is the genuinely surprising twist in this story: India’s EV registrations are not stalling at all — quite the opposite. Data from JMK Research shows India's EV market grew 43% year-on-year in the first half of 2026, with over 1.54 million units registered between January and June, taking overall EV penetration in new vehicle sales to 11.43%, up from roughly 8% a year earlier.

Some segments moved even faster: electric three-wheeler passenger penetration reached nearly 74%, electric car sales rose 83% year-on-year, and electric truck sales — admittedly from a tiny base — surged almost 340%, from 139 units to 611.

That is precisely what makes the ceiling argument so striking. Registration counts and energy-mix share are measuring two different things, and the gap between them is the story: India can post 43% unit growth and eight new electric car launches in a single half-year, and electricity’s share of the country's actual transport energy consumption still barely moves, because two- and four-wheelers, the categories with the largest energy footprint per vehicle, remain the slowest to electrify relative to their weight in the fleet.

Registration-count optimism and energy-mix pessimism can both be true at once — and Indian policymakers have mostly been talking about the former.

“We have spent six years proving that subsidies alone can move the needle on segments like buses and autos where procurement is centralised, but not on the mass consumer market,” said a senior official at a central government ministry involved in transport policy. “Delhi's policy is really a test of whether India is willing to make electrification compulsory rather than optional.”

Why the subsidy model hit a ceiling

The Down To Earth analysis offers a genuinely underexplored explanation for why Delhi felt compelled to make this shift, and it goes well beyond air-quality politics.

Segments where India mandated adoption through public procurement or permit structures — electric buses, three-wheelers — have electrified rapidly: Delhi’s bus fleet is now 79% electric, and three-wheeler passenger BEV penetration has reached 35% nationally, touching 92% in Assam and 98% in Jammu and Kashmir.

But segments left to consumer choice and subsidy alone have stalled.

National two-wheeler BEV penetration sits at just 6.3%, with Honda, Yamaha and Royal Enfield recording zero battery-electric sales in 2025-26. Cabs fared worse still, at 1.6% nationally, with Maruti — the largest player in that segment — selling no BEVs at all.

Delhi's own two-wheeler adoption actually slowed when subsidy support under the central EMPS scheme was reduced, then only partially recovered.

That pattern is the underexplored standout insight in this story: India's EV boom, so often described as a single national trend, is really two entirely separate transitions moving at wildly different speeds — one driven by regulation and running ahead of target, the other driven by incentives and stuck below 7%.

Delhi’s current policy is effectively an attempt to drag the second group into the first by making non-compliance commercially impossible rather than merely financially unattractive.

The pushback and the precedent

The pushback and the precedent

Automakers, unsurprisingly, are uneasy. A Morgan Stanley note on the policy argues Delhi’s own market is too small to hurt manufacturers directly — consumers can simply register vehicles in neighbouring states — but warns that the real risk is replication.

Chandigarh had earlier proposed its own ICE two-wheeler ban before deferring implementation to 2027 under industry pressure, a preview of the resistance likely to greet any state that follows Delhi’s lead. The brokerage flagged the motorcycle segment, where credible electric alternatives remain thin, as the likeliest flashpoint, while noting that manufacturers with established EV portfolios, such as Hero MotoCorp, Bajaj Auto and TVS Motor, are better placed to absorb the shift.

“Hybrid exclusion effectively tells manufacturers there is no transitional runway left — it’s full electric or nothing, on a fixed clock,” said an executive at one of India's leading two-wheeler manufacturers. “That is workable for companies that started investing early. For everyone else, the compliance timeline is genuinely tight.”

The diffusion Morgan Stanley warned of is already underway, if quietly. Bihar has amended its own EV policy to target 30% EV penetration in new vehicle registrations by 2030 — a softer, incentive-led version of Delhi's ambition rather than a hard registration ban, but still evidence that state governments are treating Delhi's framework as a reference point rather than an outlier.

Whether other large vehicle markets — Maharashtra, Karnataka, Uttar Pradesh — follow with binding mandates of their own, rather than aspirational targets, is likely to matter more for India's 2030 electrification trajectory than anything Delhi does within its own borders.

The global mandate playbook, and its limits

Delhi’s regulatory turn puts India in company with a small set of jurisdictions that have tried to force EV adoption through binding manufacturer or registration obligations rather than demand-side sweeteners.

California’s Zero-Emission Vehicle mandate, dating to 1990, is widely credited with forcing sustained EV investment decades before subsidies existed; even as it now faces federal legal challenge, the market transformation it seeded has proven durable.

China’s own New Energy Vehicle credit mandate pushed NEV penetration past 51% of new car sales in 2025, and Beijing is now tightening rather than loosening the scheme’s technical thresholds.

The European Union offers the cautionary counter-example: its original 2035 combustion-engine phase-out, once a genuine driver of battery investment, was diluted in late 2025 to a 90% emissions-reduction target under industry lobbying — exactly the outcome a regulation-led strategy is designed to avoid, and a fate Delhi’s three-year resale lock-in appears engineered to forestall.

Beijing’s view from the outside

There is a further, rarely discussed angle to India’s EV story: how it looks from China. Chinese industry commentary, according to a report, increasingly frames India’s EV expansion not as competitive pressure but as a demonstration of continued dependency.

Chinese analysts note that more than 90% of the battery cells used in Indian EVs are still imported, with China dominating lithium-ion cells, cathode materials and core manufacturing technology across the value chain.

In that reading, India’s EV sector remains largely an assembly operation, its manufacturing ambitions bounded by the very supply chains Delhi’s mandates cannot touch. It is a useful corrective to the assumption that faster registration numbers automatically translate into strategic autonomy — the two are, for now, running on separate tracks.

What the next four years will decide

None of this diminishes what India has achieved: a bus fleet approaching full electrification in the capital, three-wheeler segments electrifying faster than almost anywhere in the world, and a battery-demand trajectory expected to rise from around 17.7 GWh in 2025 to 256.3 GWh by 2032 — a compound growth rate of roughly 35% a year.

But that demand curve exposes the weakest link in the entire strategy. As of late 2025, only around 1.4 GWh of cell manufacturing capacity was operational under the government’s PLI-ACC battery scheme, against a 50 GWh target.

Until that capacity gap closes, every registration mandate Delhi or any other state imposes effectively manufactures demand for cells that India still has to import — which is exactly the dependency Chinese commentators point to when they describe India’s EV sector as an assembly operation rather than a manufacturing one.

That is the uncomfortable symmetry at the heart of this story: a registration mandate can force a two-wheeler company to sell electric, but it cannot, on its own, force a battery cell into existence on Indian soil.

Closing the ₹12.5-lakh-crore (US$129.8 billion) investment gap will therefore mean two simultaneous transitions — regulatory, to pull reluctant OEMs and consumer segments into electrification, and industrial, to build the cell-manufacturing base that makes that electrification something more than an import-substitution exercise in reverse.

Whether Delhi's regulation-first model survives contact with an anxious auto industry, whether other states follow with mandates rather than mere targets, and whether battery localisation keeps pace with registration growth, will together do more to determine India's 2030 electrification outcome than any single subsidy scheme has managed in the past six years.