India's electric vehicle industry is enjoying what many executives describe as a breakthrough moment. Passenger EV sales are rising sharply, global manufacturers are expanding their India plans, policymakers are preparing a fresh incentive framework, and industry estimates suggest the country's passenger vehicle sector could attract investments worth ₹3.5 lakh crore (≈ US$37 billion) over the coming decade as electrification gathers pace.

Yet beneath the optimism lies an uncomfortable question: can India build a globally competitive EV industry without relying on Chinese technology?

The question has acquired new urgency after reports that Tata Motors plans to use technology from Chinese automaker Chery for its premium Avinya electric vehicle programme. The partnership, which centres on Chery's Freelander platform, would help Tata accelerate the launch of premium EVs after delays in developing alternatives linked to Jaguar Land Rover's architecture. The first Avinya model is expected in 2027, with another likely to follow later in the decade.

At one level, the arrangement reflects a pragmatic business decision. At another, it highlights a deeper reality that policymakers and industry leaders have so far been reluctant to confront openly. India may be localising assembly, attracting investment and expanding EV manufacturing, but the technological foundations of the global EV revolution remain heavily concentrated in China.

Beyond batteries

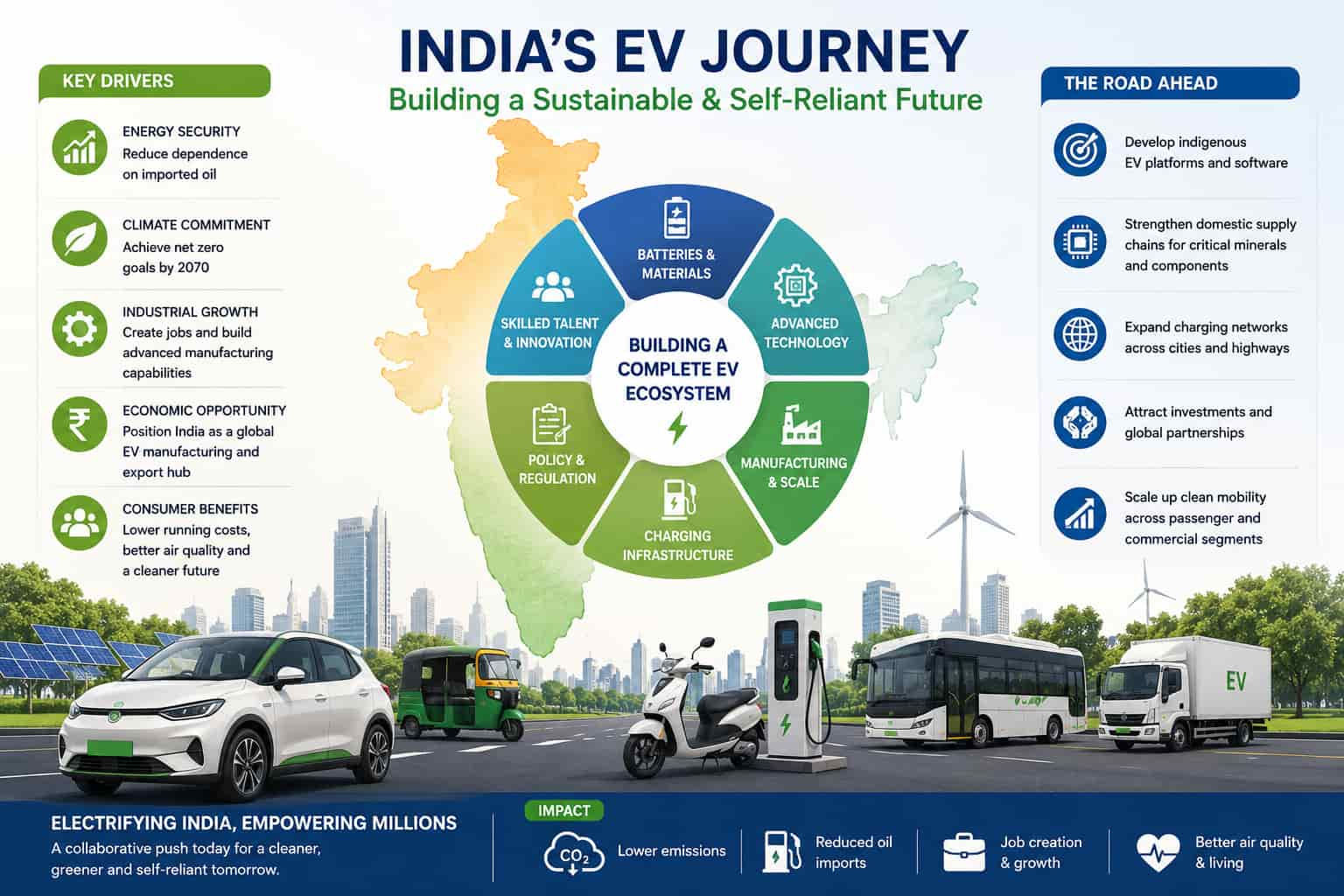

Much of India's EV strategy has focused on batteries, minerals and manufacturing incentives. Recent discussions around a new EV policy and possible import-duty concessions for companies willing to manufacture locally indicate that New Delhi is increasingly treating electric mobility as an industrial strategy rather than merely a transport policy.

The government is also reportedly considering stronger support for electric two-wheelers, a segment where India has become one of the world's largest EV markets. Yet batteries are only one layer of the EV ecosystem.

The next battleground is software-defined vehicles, advanced electronics, vehicle operating systems, digital architectures and integrated mobility platforms. Increasingly, the world's most competitive EVs are not merely cars powered by batteries; they are software platforms on wheels.

This is precisely where China has established a commanding lead.

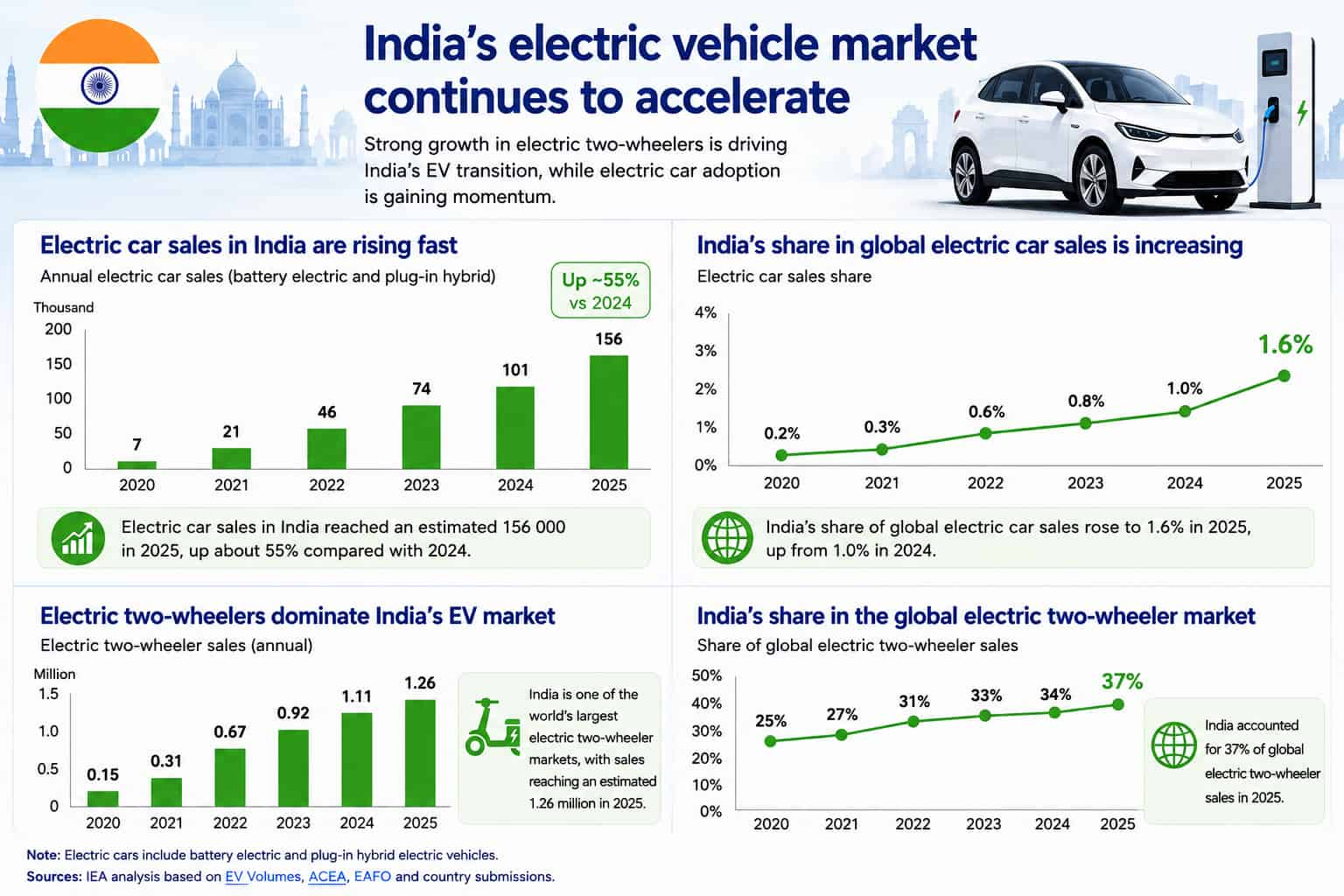

According to the International Energy Agency's Global EV Outlook 2026, China accounted for nearly 75% of global EV production in 2025, produced more than 80% of global battery cells, and dominates battery materials and supply chains. Chinese manufacturers exported more than 2.5 million electric vehicles last year, while Chinese battery producers continue to expand their global footprint.

What is less appreciated is that China is increasingly exporting something even more valuable than vehicles: technology platforms.

The Chery-Tata arrangement illustrates this shift. Rather than investing directly in Indian manufacturing, Chinese companies are increasingly licensing vehicle architectures, engineering systems and EV platforms to overseas manufacturers. The model resembles how global technology firms license software rather than hardware.

The paradox of self-reliance

India's EV ambitions are rooted partly in reducing dependence on imported oil and strengthening industrial self-reliance.

However, there is a growing risk that the country could replace one strategic dependence with another.

For decades, India's transport sector depended heavily on imported crude oil. Tomorrow's mobility economy could depend on imported battery technologies, software systems, semiconductors and EV platforms.

The irony is that India's localisation success may actually increase this risk. As EV adoption accelerates, manufacturers face intense pressure to launch products quickly and at competitive prices. Building proprietary platforms from scratch requires years of development and billions of dollars in investment. Licensing proven Chinese technology often appears cheaper, faster and commercially less risky.

Industry analysts note that China's advantage today resembles Japan's position in automobiles during the 1980s or South Korea's position in electronics during the 2000s. The difference is that EV technology cycles are moving far faster, making it difficult for late entrants to catch up.

A global pattern is emerging

India is not alone. Chinese EV makers and technology providers are expanding rapidly across Europe, Southeast Asia, Latin America and the Middle East.

The United Kingdom, for example, has witnessed rapid growth in sales of Chinese EV brands such as Chery, BYD and Geely. Chinese models are increasingly competing directly with established Western manufacturers in markets that were once considered difficult to penetrate.

This reflects a broader transformation in global automotive competition.

For much of the twentieth century, carmakers competed through engines, manufacturing efficiency and brand strength. In the EV era, competitive advantage increasingly rests on batteries, software, artificial intelligence, power electronics and digital ecosystems.

According to the IEA, software-defined vehicles are becoming a defining feature of the industry, with EV manufacturers leading the transition towards centralised software systems, remote upgrades and AI-enabled vehicle management.

China currently leads many of these areas.

The overlooked freight opportunity

Another surprising lesson emerges from global EV trends.

India's public conversation remains heavily focused on passenger cars. Yet internationally, some of the fastest progress is occurring in commercial transport.

The IEA reports that global electric truck sales more than doubled in 2025, with China accounting for most of the growth. One in four trucks sold in China last year was electric.

This raises an important question for India.

If the country's objective is energy security and oil-import reduction, electrifying freight corridors, logistics fleets and commercial transport could potentially deliver greater economic benefits than subsidising additional passenger-car purchases.

Several entrepreneurs are already betting on this shift, arguing that freight electrification may become the next major phase of India's mobility transition.

What happens next?

India's EV market is undoubtedly accelerating.

The IEA estimates that electric-car sales globally could reach 23 million units this year. In India, electric two-wheeler sales continue to grow strongly, while passenger EV adoption is beginning to move beyond early adopters.

But the next phase of the transition will be less about sales volumes and more about technological sovereignty.

India has already recognised the importance of securing critical minerals, supporting battery manufacturing and attracting EV investment. The harder challenge may be building indigenous capabilities in vehicle software, advanced electronics, powertrain architectures and next-generation mobility platforms.

The Tata-Chery partnership is therefore more than a corporate arrangement. It is an early glimpse of a strategic dilemma that many countries will face during the energy transition.

The question is no longer whether India can build electric vehicles.

The question is whether India can build the technologies that make those vehicles competitive in a world increasingly shaped by Chinese innovation.

That answer may determine whether India becomes merely a large EV market or emerges as a genuine global EV power.