India’s electric vehicle (EV) story is no longer just about adoption curves and subsidy-led demand. A new phase is unfolding—one that is less visible but far more consequential.

As policy signals tighten, infrastructure rules harden, and systemic risks come into focus, India appears to be shifting from a market-driven EV expansion to a strategically governed transition.

The developments emerging over the past few months—from localisation-linked subsidies for electric trucks to mandatory charging infrastructure in buildings—suggest that the country is beginning to treat EVs not merely as a clean mobility solution, but as a strategic industrial and energy system.

From demand push to supply-side control

For years, India’s EV push relied on demand-side incentives such as the Faster Adoption and Manufacturing of Electric Vehicles (FAME) scheme and state subsidies. That phase is now giving way to a more assertive policy approach focused on domestic manufacturing and supply chain control.

The government’s move to link EV truck subsidies to the localisation of key components, expected to come into effect from September 2026, marks a clear inflection point. The tightening of norms around component sourcing is aimed at boosting domestic manufacturing of critical parts such as batteries, motors, and power electronics.

This shift reflects a growing concern within policymaking circles: that India’s EV boom could replicate the trajectory of solar energy, where rapid deployment led to heavy dependence on imports—particularly from China.

“India is learning from past transitions,” said an industry executive familiar with policy discussions. “The emphasis now is not just on how many EVs are sold, but on who controls the value chain behind them.”

Demand is rising—but no longer the core challenge

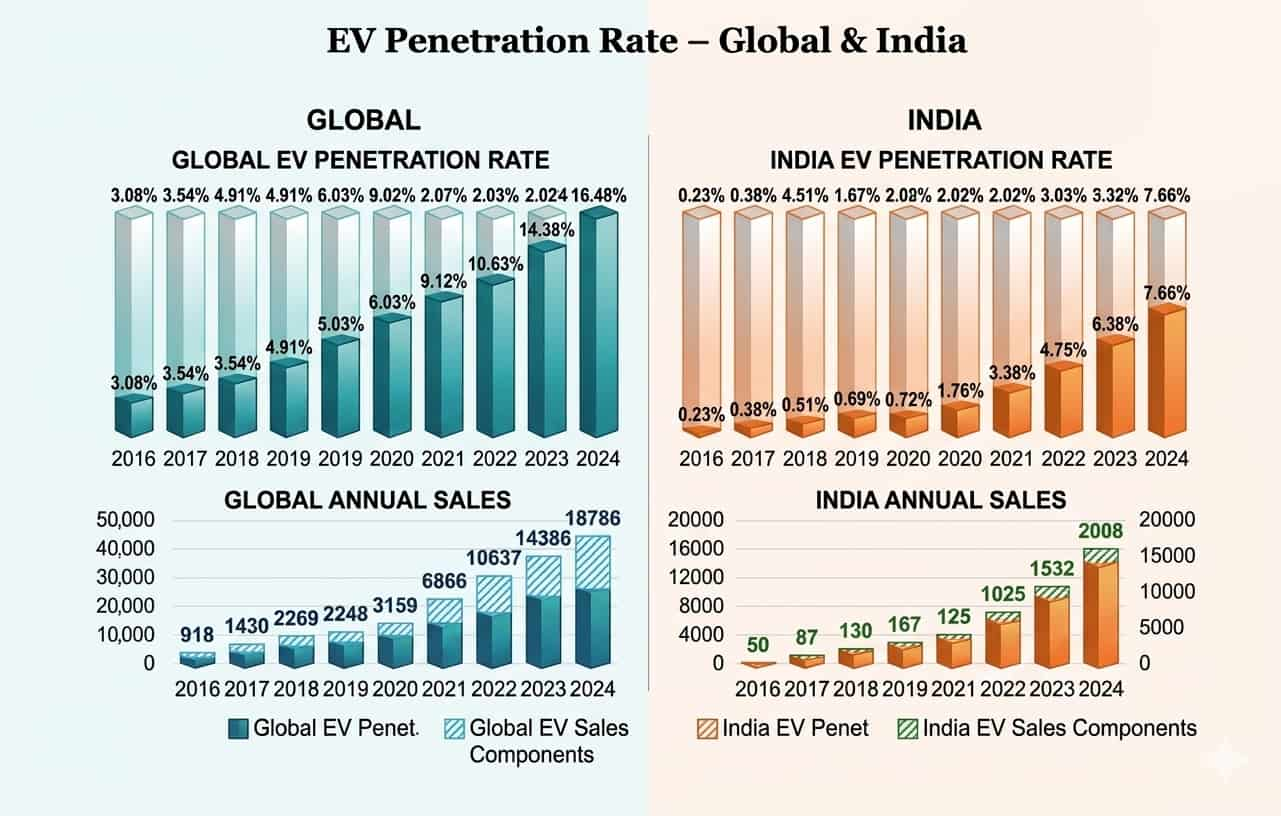

Paradoxically, this tightening of policy comes at a time when EV demand is accelerating sharply. Electric car sales in India rose by nearly 70% during the January–April period this year, signalling growing consumer acceptance and improved market viability.

State-level incentives, expanding product choices, and rising fuel costs have all contributed to this surge. States continue to play a critical role in shaping EV markets through targeted subsidies, tax exemptions, and infrastructure support.

However, policymakers increasingly recognise that demand is no longer the primary bottleneck. The more pressing challenge lies in ensuring that this demand is supported by a robust, resilient, and domestically anchored ecosystem.

Charging infrastructure becomes a regulatory layer

One of the most visible shifts is in how EV charging infrastructure is being treated. What was once seen as a private investment opportunity is now evolving into a regulated public utility layer.

Haryana’s proposal to mandate EV charging infrastructure in new buildings signals a move towards embedding EV readiness into urban planning itself. Telangana, meanwhile, has invited landowners to participate in setting up charging stations, extending deadlines to accelerate participation.

At the same time, concerns are emerging about the resilience of charging infrastructure under extreme conditions. Questions are being raised about whether India’s EV charging network is equipped to handle temperatures exceeding 50°C—conditions increasingly common due to climate change.

These developments indicate a deeper shift: EV infrastructure is no longer peripheral—it is becoming central to urban policy, grid planning, and climate resilience.

The emerging layer of systemic risks

As EV adoption deepens, a new set of risks is coming into view—risks that extend beyond the traditional concerns of cost and infrastructure.

Cybersecurity has emerged as a particularly sensitive issue. Concerns have been raised about the potential vulnerabilities associated with connected EV systems, especially those linked to foreign manufacturers. The possibility that EVs could serve as data collection nodes or even vectors for cyber intrusion has begun to feature in strategic discussions.

At the same time, the integration of EVs into the power grid introduces new complexities. Large-scale EV adoption could significantly alter demand patterns, requiring grid upgrades, smarter load management, and enhanced storage capacity.

“Electric vehicles are no longer just transport assets,” noted a senior energy analyst. “They are becoming mobile nodes in a much larger energy and data ecosystem.”

The missing link: Ecosystem scale

Despite rapid progress, a recurring theme across industry analyses is the absence of a fully developed EV ecosystem. A recent assessment by Nomura emphasised the need for a China-style ecosystem push, combining scale, policy coordination, and infrastructure investment.

China’s success in EVs has been underpinned not just by demand incentives but by a comprehensive industrial strategy encompassing battery manufacturing, supply chains, charging infrastructure, and technological innovation.

India is beginning to move in a similar direction, albeit with its own constraints and priorities.

Battery storage is emerging as a critical component of this ecosystem. Companies such as Adani Green Energy are planning to add up to 15,000 GWh of battery energy storage capacity annually, signalling a growing recognition of the need for grid flexibility.

At a broader level, countries across the Asia-Pacific region—including India, Australia, Japan, and the Philippines—are driving a shift towards battery storage as a key enabler of energy transitions.

Global context: A race for control, not just adoption

India’s evolving EV strategy mirrors a broader global trend. Across major economies, EV policies are increasingly shaped by concerns around supply chain security, technological sovereignty, and geopolitical competition.

The United States has introduced localisation requirements under the Inflation Reduction Act. The European Union is pushing for domestic battery manufacturing through initiatives like the European Battery Alliance. China continues to dominate global EV supply chains, leveraging its control over critical minerals and manufacturing capacity.

In this context, India’s push for localisation and ecosystem development appears less like a policy choice and more like a strategic necessity.

Counterarguments: Risks of overregulation

While the shift towards tighter control has clear strategic logic, it also raises concerns.

Industry stakeholders caution that excessive localisation requirements could increase costs, slow down innovation, and deter investment—particularly in the early stages of market development.

There are also questions about whether India can realistically replicate China’s ecosystem model, given differences in scale, state capacity, and industrial structure.

“Policy certainty is crucial,” said a senior executive at an EV startup. “If regulations become too restrictive or unpredictable, it could undermine the very growth they are trying to support.”

What lies ahead: The next phase of India’s EV transition

Looking ahead, India’s EV trajectory is likely to be shaped by how effectively it navigates this transition from growth to governance.

Three trends are likely to define the next phase:

1. Deepening localisation: Expect further tightening of norms around domestic manufacturing, particularly in batteries and critical components.

2. Infrastructure as policy: Charging infrastructure will increasingly be integrated into urban planning, building codes, and public investment frameworks.

3. Integration with the energy system: EVs will become more closely linked with renewable energy, storage, and grid management, transforming them into active participants in the energy ecosystem.

Beyond electrification

India’s EV journey is entering what may be its most decisive phase yet. The easy gains from subsidies and early adoption are giving way to more complex challenges of scale, control, and resilience.

What is emerging is not just an electrification of mobility, but a broader reconfiguration of how mobility systems are designed, governed, and integrated with the economy.

In this new phase, the key question is no longer how fast EVs can grow—but how strategically they can be embedded within India’s industrial and energy landscape.

Cover image: AI-generated (representative)