India’s energy story is no longer about ambition—it is about execution under pressure. A series of recent developments across renewable capacity, manufacturing, global trade tensions and investment flows suggest that the country has crossed an inflection point.

The transition away from fossil fuels is no longer theoretical. It is happening. But the deeper story emerging from the latest data and policy signals is far more complex: India is entering a phase where the energy transition is shaped as much by geopolitics, finance and structural inefficiencies as by technology.

Taken together, recent reports—from renewable generation trends to trade disputes and investment surges—paint a picture of a system in motion, yet under strain.

A turning point: Renewables begin to displace fossil fuels

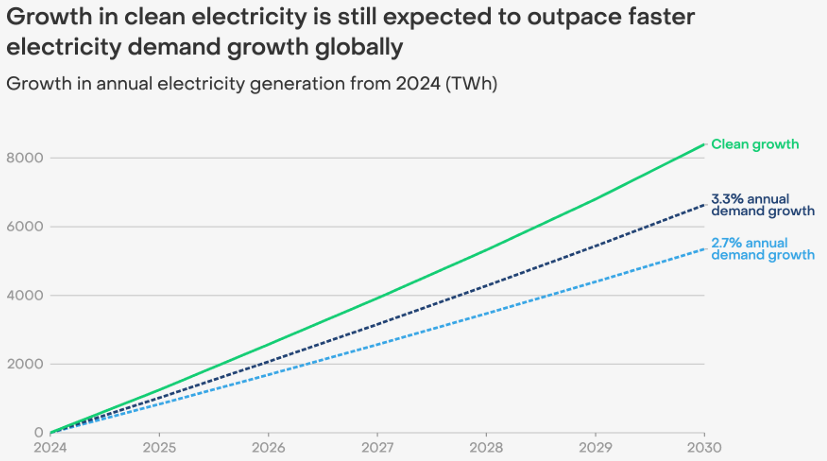

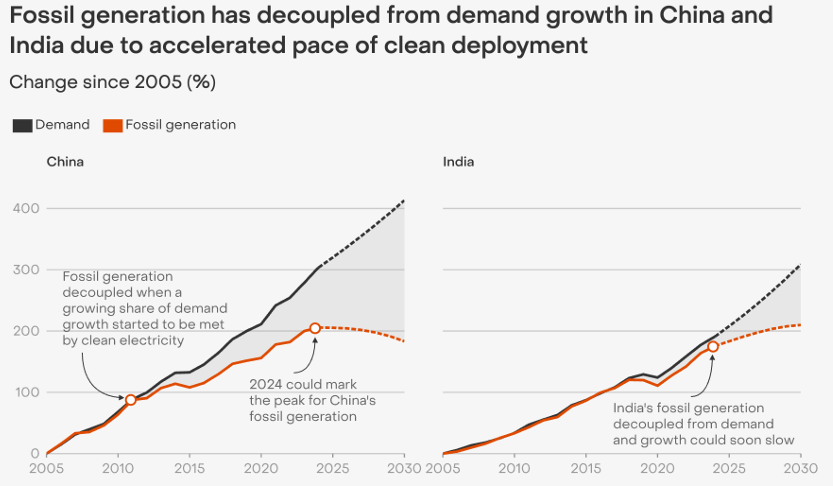

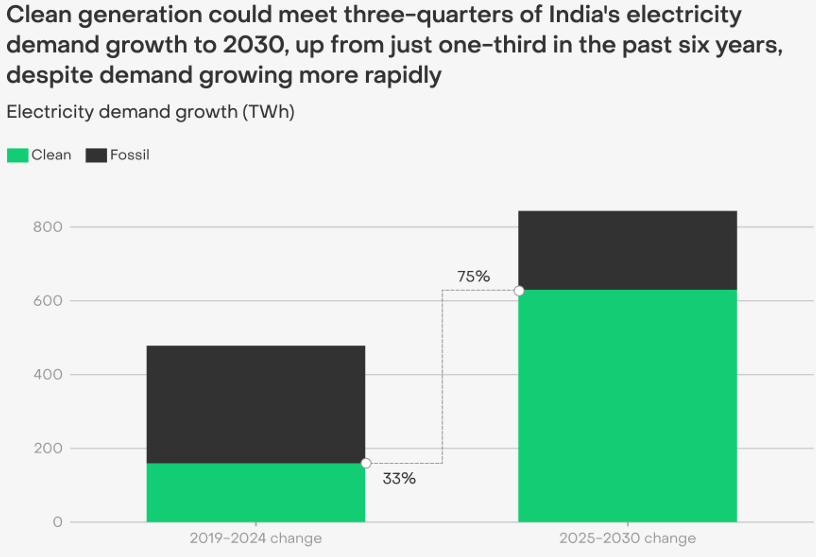

For the first time, India’s renewable expansion is not just adding to the grid—it is beginning to replace fossil fuel generation. According to recent estimates, fossil fuel-based electricity generation declined by around 3.3% in 2025, even as overall demand continued to grow. This shift, driven by a surge in solar and wind output, marks a structural transition in the power sector rather than a cyclical fluctuation.

This development is significant because India’s power demand has historically been met by scaling up coal-based generation. The emerging trend suggests a subtle but important reversal: renewables are beginning to absorb incremental demand growth.

However, there is a caveat. Part of this decline in fossil generation is also linked to relatively slower demand growth in the past year. Analysts caution that this does not yet represent a permanent decoupling. “The real test will come when demand spikes again—whether renewables can consistently absorb that growth,” said an official from a power major familiar with grid data.

Source: EMBER | Global Electricity Review 2025

Manufacturing push meets global headwinds

India’s ambition to become a global solar manufacturing hub is gaining momentum. Companies are moving into higher-efficiency module production, backed by government incentives and production-linked schemes. This shift toward advanced manufacturing is critical if India wants to reduce dependence on imports and compete globally.

Yet, just as India ramps up its capabilities, global trade barriers are beginning to rise. The United States has imposed anti-dumping duties of up to 123% on certain Indian solar imports, citing unfair pricing practices.

This move underscores a growing reality: clean energy is no longer a purely cooperative global endeavour. It is increasingly shaped by protectionism and strategic competition.

For India, the implications are significant. Export markets could shrink just as domestic capacity expands, potentially leading to oversupply pressures. The country may have to pivot more aggressively toward domestic demand or explore alternative markets in regions such as Africa and the Middle East.

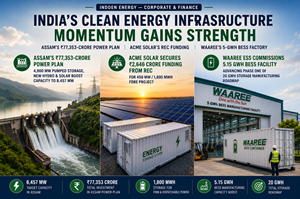

Investment boom—but not without risks

Another striking development is the surge in renewable energy deal activity. India’s renewable energy deal value reportedly jumped fivefold to around $2 billion in 2025, signalling strong investor interest in the sector.

This surge reflects confidence in long-term policy direction and growing demand for clean energy assets. However, beneath this optimism lies a structural challenge: the cost of capital in India remains significantly higher than in developed markets.

Higher financing costs can erode the competitiveness of renewable projects, especially when tariffs are tightly regulated. “India’s transition is capital-intensive, and the cost of that capital will determine how fast and how smoothly the transition unfolds,” said an industry executive involved in project financing.

Moreover, increased deal activity does not automatically translate into efficient deployment. Delays in land acquisition, grid connectivity issues and payment risks from distribution companies continue to weigh on the sector.

The missing pillar: Energy efficiency

While much of the focus has been on adding renewable capacity, policy experts are increasingly emphasising the importance of energy efficiency. At first glance, calls to “reduce demand growth” can seem counterintuitive in a country like India, where energy consumption remains well below that of advanced economies and must rise to support development.

However, the concern is not about limiting demand itself, but about improving the quality of that growth. In practice, a significant portion of rising demand is driven not by new economic activity, but by inefficiencies—outdated technologies, poorly designed buildings, and high transmission and distribution losses. Left unaddressed, this inflates the energy requirement without delivering proportional economic or social value.

Energy efficiency, therefore, offers a less visible but highly impactful pathway to decarbonisation. By reducing waste and optimising usage, it lowers the need for additional capacity, eases pressure on the grid, and improves system resilience—without constraining legitimate consumption.

Crucially, these gains extend beyond end-use efficiency. Improvements in transmission infrastructure and grid technology—such as modernised networks and smarter load management—can significantly cut technical losses and optimise power flows.

In effect, a more efficient grid can ‘create’ usable power by ensuring that more of what is generated actually reaches consumers.

This introduces a critical counterpoint to the prevailing narrative. The transition is not just about building more solar parks or wind farms—it is about rethinking both how energy is consumed and how it is delivered. Without this shift, India risks entering a cycle of overbuilding capacity while still struggling with supply-demand mismatches.

Source: EMBER | Global Electricity Review 2025

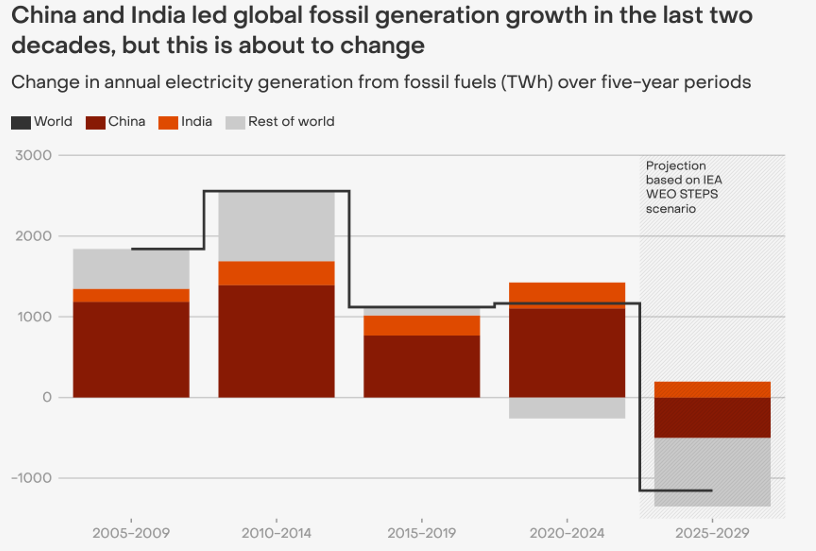

Coal’s enduring role

Despite rapid renewable growth, coal continues to play a central role in India’s energy mix. It remains the backbone of baseload power, ensuring grid stability during periods of variability in renewable output.

Recent trends indicate that while coal’s share may gradually decline, its absolute consumption is unlikely to drop sharply in the near term. This reflects the dual challenge India faces: meeting rising energy demand while transitioning to cleaner sources.

This duality is often overlooked in global discussions. Unlike developed economies with stable or declining demand, India must expand its energy system even as it decarbonises. This makes the transition inherently more complex.

The geopolitics of green energy

One of the most striking themes emerging from recent developments is the growing geopolitical dimension of clean energy. Trade disputes, supply chain dependencies and strategic competition are beginning to shape the trajectory of the transition.

The imposition of tariffs on Indian solar exports is part of a broader trend where countries are seeking to protect domestic industries and secure supply chains. This mirrors earlier phases of globalisation in sectors such as oil and semiconductors.

For India, this means navigating a delicate balance. On one hand, it must build domestic manufacturing capabilities. On the other, it must remain integrated with global markets to access technology and capital.

“The energy transition is no longer just an environmental agenda—it is an industrial and geopolitical contest,” a policy expert at Deloitte tracking global energy trends told Indoen Energy.

Source: EMBER | Global Electricity Review 2025

A system under stress

As India accelerates its transition, structural weaknesses in the energy system are becoming more visible. Distribution companies continue to face financial stress, which affects their ability to purchase power and pay generators on time.

Grid infrastructure is also under pressure, as the integration of intermittent renewable sources requires significant upgrades in transmission and storage capacity.

These challenges highlight a key reality: the transition is not just about generation. It requires a comprehensive overhaul of the entire energy ecosystem—from production and transmission to distribution and consumption.

The road ahead: Balancing Ambition with reality

India’s energy transition is entering a decisive phase. The country has demonstrated that large-scale renewable deployment is possible. It has also shown that policy support and investor interest can align to drive growth.

However, the next stage will be more demanding. It will involve managing trade tensions, improving financial viability, strengthening infrastructure and addressing systemic inefficiencies.

There are also competing narratives. Optimists point to declining renewable costs and technological advancements as reasons for confidence. Sceptics highlight persistent challenges such as grid instability, financing constraints and geopolitical risks.

Both perspectives are valid. The transition is neither a linear success story nor a looming failure. It is a complex process shaped by multiple, often conflicting forces.

Source: EMBER | Global Electricity Review 2025

From transition to transformation

The most important takeaway from recent developments is that India’s energy transition has moved beyond the stage of intent. It is now a lived reality, with tangible impacts on generation patterns, investment flows and policy priorities.

But this progress comes with new challenges. The transition is no longer just about adding clean energy—it is about managing a system in flux.

The real battle, therefore, is not about whether India will transition, but how it will navigate the competing pressures of growth, sustainability and geopolitical uncertainty.

In that sense, India is not just decarbonising its economy. It is negotiating its place in a rapidly evolving global energy order.

Cover image: AI-generated (representative)