In March 2026, India signalled a major shift in its clean-energy strategy when policymakers began pushing for stricter domestic sourcing rules for solar manufacturing inputs such as wafers and ingots — components that form the technological backbone of photovoltaic panels.

The move reflects a deeper strategic concern: that India’s clean-energy future cannot depend indefinitely on imported technology.

At nearly the same time, major industrial groups were making their own bets. Reliance Industries expanded its clean-energy manufacturing ambitions while securing long-term green ammonia export agreements, part of a broader push to build an integrated clean-technology ecosystem spanning solar modules, batteries and hydrogen systems.

These developments may appear disconnected. But together they illustrate a deeper shift underway in India’s energy transition. The real story is no longer just about installing renewable energy capacity. It is about whether India can also manufacture the technologies that power that transition.

This raises a question that could shape the country’s economic future: can India transform its clean-energy demand into an industrial revolution similar to what information technology achieved in the early 2000s?

From energy transition to industrial strategy

For more than a decade, India’s clean-energy story has been dominated by deployment milestones. Solar parks expanded. Wind installations grew. Electric mobility gained policy momentum.

But a quieter policy realisation is now emerging. Energy transition without manufacturing leadership may reduce emissions, but it does not automatically create industrial power.

India currently imports a significant share of key clean-technology inputs, especially in solar cells, battery components and critical minerals. This dependence has begun to worry policymakers who remember how fossil-fuel imports exposed the economy to geopolitical shocks and price volatility.

The fear is simple: India must not replace oil dependence with technology dependence. This is why the conversation is increasingly shifting from gigawatts to supply chains.

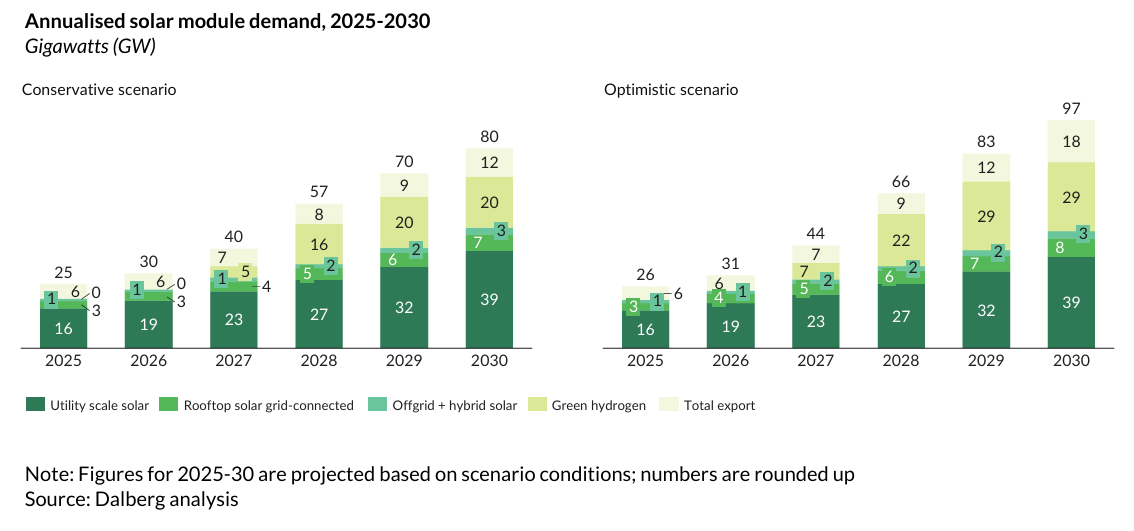

The demand wave that could reshape Indian industry

The scale of India’s future demand for clean technologies is staggering.

Electricity demand is expected to more than double over the coming decades as industrial electrification accelerates, cooling demand rises due to climate change, and electric vehicles expand into mainstream transport.

Meeting these needs requires not only renewable generation but also batteries, grid equipment, electrolysers, hydrogen infrastructure and advanced transmission systems.

This demand could create one of the largest cleantech markets in the world. The question is whether India will remain primarily a buyer in this market or become a producer.

If domestic firms capture even a fraction of this value chain, the economic implications could be transformative. Manufacturing tends to generate clusters of suppliers, technical services, logistics providers and research ecosystems.

History shows that countries that manufacture critical technologies often gain economic advantages that extend far beyond the original sector.

Jobs: The political economy of cleantech manufacturing

The employment dimension may be even more significant than the industrial one.

India faces the continuing challenge of generating large numbers of productive jobs. Service-sector growth alone may not absorb the country’s expanding workforce. Manufacturing, particularly in emerging technology sectors, offers one possible solution.

Clean-technology manufacturing spans a wide skill spectrum. Assembly operations require technicians. Equipment manufacturing requires precision engineers. Materials processing requires chemical specialists. Logistics networks require operational expertise.

This diversity makes cleantech manufacturing particularly attractive as a job creator.

Moreover, manufacturing tends to disperse geographically. Unlike digital services concentrated in major cities, manufacturing clusters often emerge in tier-two industrial regions.

This could make cleantech manufacturing not only an economic strategy but also a regional development strategy.

India’s early progress — and structural gaps

There are signs of progress. Government incentives have helped domestic solar module manufacturing capacity expand rapidly over the past few years. Installed module capacity has grown dramatically since the early 2020s, reflecting policy support and investor interest.

Yet beneath this progress lies a structural weakness.

India remains stronger in downstream assembly than upstream manufacturing. High-value segments such as polysilicon, wafers and advanced materials remain limited domestically.

This imbalance matters because the greatest technological control and profit margins often lie upstream.

Without developing these segments, India risks assembling imported components rather than building fully integrated industrial capability.

The innovation constraint

Another structural constraint is innovation capacity.

Research and development spending remains relatively modest compared with major manufacturing competitors. Countries that dominate cleantech manufacturing today invested heavily in research ecosystems decades earlier.

Innovation is not just about inventing new technologies. It is also about improving manufacturing processes, reducing costs and developing intellectual property advantages.

Without sustained R&D investment, India may find itself competing mainly on cost rather than technological leadership.

Financing the manufacturing push

Capital requirements represent another barrier. Clean-technology factories often require billions in upfront investment. Returns may take years to materialise. In India, relatively higher borrowing costs can complicate such investments.

Even government incentives sometimes face implementation delays. Reports indicate that payouts under certain solar manufacturing incentive schemes have progressed more slowly than expected, highlighting execution risks in industrial policy.

Such delays may affect investor confidence if not addressed through better policy coordination.

Battery manufacturing: Ambition versus execution

India’s battery manufacturing ambitions illustrate both opportunity and difficulty.

The government’s advanced battery incentive programmes aimed to create significant domestic cell manufacturing capacity. However, progress has been slower than planned.

By late 2025, only a small fraction of targeted battery manufacturing capacity had become operational, reflecting delays linked to capital intensity, technology challenges and supply-chain constraints.

This gap between ambition and execution highlights a recurring theme in industrial policy: announcing incentives is easier than building factories.

Yet industry interest remains strong, with multiple companies planning gigafactories in coming years despite these early setbacks.

Industry bets on the clean manufacturing future

Despite challenges, major industrial groups are investing aggressively.

Reliance Industries is building integrated clean-energy manufacturing complexes covering solar modules, storage systems and hydrogen technologies.

Tata Power has explored expanding into upstream solar manufacturing including wafers and ingots to strengthen domestic supply chains.

Such investments suggest Indian industry sees long-term opportunity despite short-term risks.

Industrial transformations often begin with such early bets. Not all succeed. But those that do can reshape sectors.

The global manufacturing chessboard

India’s push must also be understood in a global context.

China remains the dominant player across most clean-technology supply chains due to scale advantages and early investments.

The United States has responded through massive subsidies under its Inflation Reduction Act. Europe is attempting to build domestic capacity through industrial policy frameworks.

This emerging competition reflects a broader geopolitical reality: clean technology is becoming strategic.

Countries are not only seeking clean energy. They are seeking control over the technologies that enable it.

India’s large domestic market gives it an advantage few countries possess. But capturing this advantage will require execution speed.

The China question

No discussion of cleantech manufacturing is complete without addressing China’s role.

Chinese firms dominate global solar manufacturing and maintain strong positions in battery supply chains.

Some analysts argue India cannot realistically compete with China’s scale advantages.

Others argue diversification pressures are creating opportunities. Global firms increasingly seek alternative manufacturing bases to reduce concentration risks.

India could benefit from this shift if it can offer policy stability, infrastructure readiness and skilled labour.

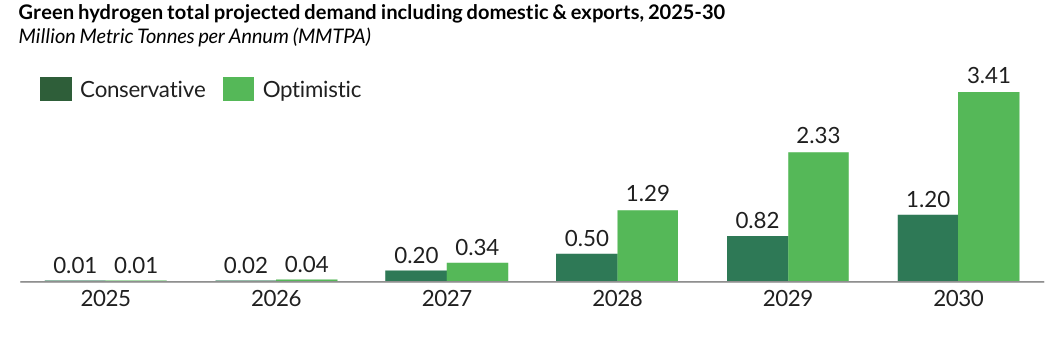

The hydrogen opportunity

Among emerging sectors, green hydrogen may offer India a chance to enter the market early.

Hydrogen is expected to play a critical role in decarbonising heavy industry and long-distance transport. Electrolyser manufacturing and hydrogen infrastructure could become major industrial sectors.

India’s advantage lies in relatively low renewable power costs, which could support competitive hydrogen production.

However, hydrogen markets remain uncertain. Costs remain high and global demand is still developing.

Early investment therefore carries both promise and risk.

The MSME ecosystem challenge

Large factories alone do not create industrial ecosystems.

They require supplier networks of smaller firms providing components and services.

India’s MSME sector could play a crucial role if integrated effectively into cleantech supply chains.

However, smaller firms often face barriers including technology access, financing and quality certification.

Without deliberate integration strategies, the benefits of cleantech manufacturing may remain concentrated among large players.

A turning point in the policy conversation

It is within this broader industrial debate that one recent sectoral analysis, Blueprint for India’s Cleantech Manufacturing Ambition, highlighted both the economic opportunity and structural constraints facing India’s attempt to capture more domestic value from the clean-energy transition.

The analysis argued that success would depend not only on incentives but also on innovation capacity, supply-chain integration and financing reforms.

Such research reflects a growing recognition that clean-energy deployment alone does not guarantee industrial development.

The counterargument: Is localisation worth the cost?

Not everyone agrees with aggressive localisation.

Some economists argue that importing cheaper technologies may allow faster decarbonisation. Domestic manufacturing, they argue, could initially increase costs.

There is historical precedent for such concerns. Protectionist industrial policies have sometimes produced inefficient industries.

Critics also note that India’s comparative advantage has historically been stronger in services than manufacturing.

These counterarguments deserve serious consideration.

Industrial policy involves trade-offs. Strategic autonomy may come at short-term efficiency costs. The real policy question is whether long-term resilience justifies these investments.

Export potential: The long game

If India succeeds in building competitive manufacturing, exports could become a major opportunity.

Many developing countries are expected to expand renewable energy adoption over coming decades. Affordable suppliers will be needed.

India’s success in pharmaceuticals and automotive components suggests such competitiveness is possible when domestic scale is achieved.

But export success depends on reliability, quality and trade partnerships — not just price.

Skills: The overlooked bottleneck

Even if capital and policy align, workforce readiness may determine outcomes.

Clean manufacturing requires specialised technical skills. Battery chemistry, power electronics and hydrogen engineering require capabilities not widely available.

Industry frequently reports skill mismatches between graduates and manufacturing needs.

Bridging this gap may require industry-academic partnerships and modernised technical education.

Without such efforts, talent shortages could slow growth.

Climate leadership through industry

India’s manufacturing push also has diplomatic implications.

As a major developing economy, India has argued for climate transitions that support development rather than constrain it.

Building domestic cleantech industries could strengthen this narrative by demonstrating that decarbonisation can align with economic growth.

This could enhance India’s influence among emerging economies facing similar development pressures.

Execution risks remain the biggest test

If ambition defines the opportunity, execution defines the outcome.

India’s industrial history shows that policy intent does not always translate into industrial success.

Successful manufacturing ecosystems require: policy stability, infrastructure readiness, investor confidence and administrative coordination.

Fragmented implementation can undermine strong strategies.

The next decade may determine whether India can sustain the consistency required.

The decade that may define India’s industrial future

Rarely do countries get moments when domestic demand, global supply-chain shifts and policy alignment converge.

India may be experiencing such a moment.

Clean-energy demand is rising rapidly. Global supply chains are diversifying. Domestic policy is supportive. But these windows do not remain open indefinitely.

If India builds capacity quickly, it could become a major clean-technology manufacturing hub. If not, supply chains may stabilise elsewhere.

Beyond energy: The real stakes

Ultimately, this debate is not just about solar panels or batteries. It is about whether India can convert its market scale into industrial strength.

It is about whether the clean-energy transition becomes merely an environmental story or also an economic transformation.

It is about whether the next phase of India’s growth will be defined by technology creation rather than technology consumption. History suggests countries that manufacture transformative technologies often gain lasting advantages.

India’s cleantech gamble is therefore not simply about energy. It is about the foundations of its next economic era.

And the outcome may depend less on how many solar parks India builds than on how many factories it successfully brings to life.